The automotive trade landscape is facing a structural stress test. In a push to rewrite the integration of the North American supply chain, administration negotiators are proposing a requirement that 50 percent of a vehicle's components and materials, by value, originate from U.S. sources to qualify for preferential tariff treatment under the U.S.-Mexico-Canada Agreement (USMCA). With the U.S. and Mexico having just wrapped their first bilateral negotiating round covering economic security and rules of origin for key industrial goods, the policy environment for Consumer Discretionary stocks is heavily rewarding localized production while penalizing import reliance.

Automakers are already navigating a precarious border dynamic. U.S. manufacturers have confronted over $10 billion in border duties on imports from Canada and Mexico that threaten to snarl supply chains, inflate component pricing, and aggressively squeeze factory-level margins . The stakes of this proposed overhaul go far beyond standard tariff bluster—it strikes at the core of how legacy brands build vehicles.

Margin Compression vs. Domestic Premiums

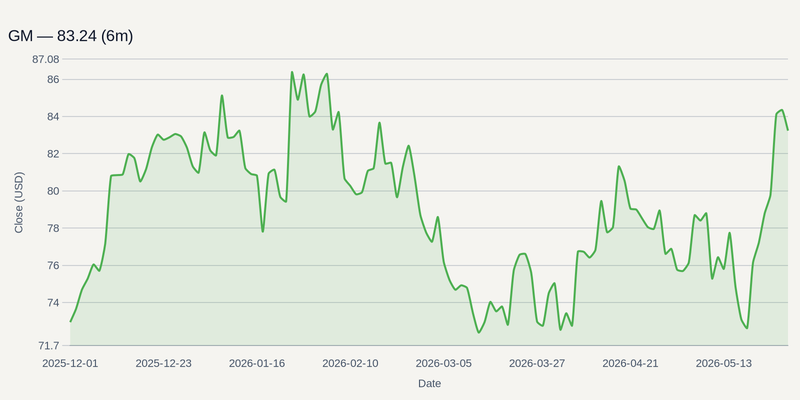

For major original equipment manufacturers (OEMs), the proposed USMCA shift acts as a severe sorting mechanism. Companies like F and GM benefit from deeply entrenched North American footprints and stand to leverage enacted tax incentives under the One Big Beautiful Bill Act (OBBBA) aimed at spurring domestic investment . However, their reliance on cross-border parts flow still exposes them to friction.

Conversely, TSLA enters this regime with a distinct structural advantage. Boasting a highly localized U.S. supply chain, its margins are largely insulated from the specific border duties currently rattling import-heavy peers.

The threat is exceptionally stark for European manufacturers operating in the U.S. market. Beyond North American trade adjustments, the executive branch's lingering threat to hike European Union auto tariffs to 25 percent creates a punishing bearish overhang for importers like BMWYY .

Tier-One Suppliers in the Crosshairs

While assembly plants dominate the headlines, the acute margin pressure will ultimately transmit through the parts and components sector. Global auto parts suppliers operate on razor-thin efficiency models that depend on frictionless border crossings.

Premier North American tier-one suppliers like MGA and BWA are acting as real-time barometers for the trade talks. Their earnings are tightly tethered to the final language of USMCA compliance updates and any potential exemptions granted to Mexican and Canadian factories. APTV, with its vast global supply web, faces outsized compliance friction, ensuring that administrative costs alone will bite into operating leverage this year.

Skeptics of a worst-case scenario argue that the strict 50% U.S.-sourced target is primarily an opening negotiating bid rather than a rigid boundary. In the recent past, the market has proven willing to fade absolute worst-case tariff fears, particularly following brief relief rallies after sweeping IEEPA tariffs faced legal invalidation and eventual mitigation . But relying on a watered-down deal leaves component suppliers heavily exposed to binary political risk.

The Summer Compliance Sprint

The statutory and regulatory timetable ensures this theme will dictate Automobiles flows well into the third quarter. Investors should anchor expectations to three critical flashpoints:

- June 2026: Finalization of negotiating positions by the U.S., Canada, and Mexico ahead of the formal trade review, following a period where tariff threats and exemptions have heavily dominated the automotive landscape .

- July 2026: The official launch of the first formal USMCA joint review on July 1, coupled with the scheduled July 24 expiration of the temporary Section 122 tariffs, which is expected to prompt key administrative updates regarding alternative statutory authorities and trade remedy investigations .

- August 2026: The potential transition to a cycle of annual reviews if a clean extension is not reached by the July deadline, which will continue to shape the long-term outlook for North American automotive manufacturing and the enforcement of rules of origin .

Until these rules are codified, OEMs and suppliers will be forced to operate in a defensive posture. Capital is likely to rotate away from parts suppliers with sprawling, border-agnostic networks, seeking shelter in auto names that command verified, localized production channels.