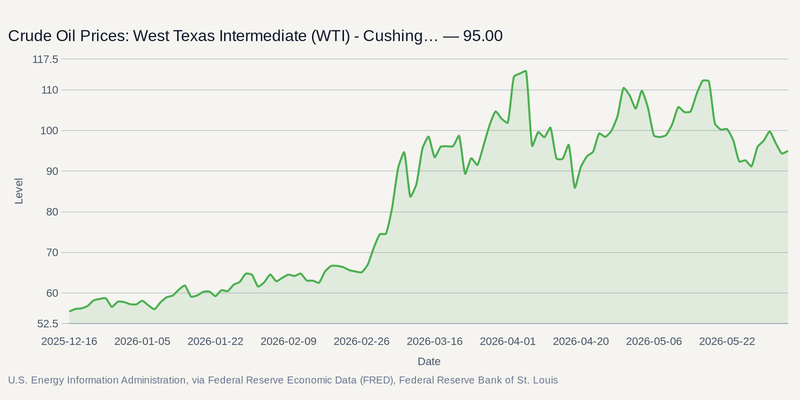

The planned reopening of the Strait of Hormuz is acting as an immediate pressure release valve for the U.S. consumer. With West Texas Intermediate crude sliding back toward $80 a barrel following a preliminary U.S.-Iran agreement, the market is aggressively repricing the threat of energy-driven demand destruction. Top-line retail momentum has not collapsed, but domestic energy costs were rapidly emerging as the potential breaking point for stretched household balance sheets .

Beneath the index-level resilience, an acute K-Shaped Consumer Spending divide is forcing corporate strategy shifts. While higher-income cohorts continue to drive a 5% to 6% nominal expansion in overall spending , structural affordability constraints are fracturing the middle and lower tiers . Relief at the pump buys these households time, but it does not erase the broader margin squeeze filtering through the retail and restaurant landscape.

The Margin Cost of Defending Traffic

Fast-food stability isn't as organic as it looks. To keep foot traffic from cratering, operators are leaning hard on margin-dilutive value deals. Q1 earnings laid bare this dependency. McDonald's and its peers rolled out aggressive meal deals to stop a bleed in lower-income visits. Data shows the hamburger segment is running nearly flat —proving that traffic is increasingly bought, not earned.

This sets up a tense July earnings cycle. Wall Street will scrutinize the profitability of these summer promotions. Historically, when operators maintain guidance while leaning entirely on deep discounts, they often trap momentum investors who mistake raw traffic for pricing power.

Trade-Down Economics and the Energy Valve

The plunge in oil prices alters the immediate trajectory for broadline retail. Discount chains and mass merchants act as the primary shock absorbers when budgets tighten. Walmart and Costco are capturing significant trade-down market share, leveraging immense supply chain scale and membership retention to defend their dominant positions. Amazon continues to straddle the divide, absorbing high-end discretionary capital while aggressively competing for the value-seeking shopper.

Conversely, retailers heavily exposed to the pure mid-tier consumer, such as Target, face a narrower path. A sustained drop in transportation and logistics costs—spurred by the anticipated reopening of Middle East shipping lanes—provides crucial breathing room to defend margins while adjusting inventory to match this trade-down behavior. For deep-value players like Dollar General, which serve the most acutely pressured demographics, relief at the gas pump acts as a direct injection into their customers' discretionary wallets.

Navigating the Summer Retail Gauntlet

The structural demand destruction that many analysts feared has not materialized, supported in part by steady employment income growth and targeted seasonal tax refunds . Even so, the fundamental reckoning for margins relies entirely on how well companies balance volume and price. Brands with unyielding pricing power, such as Chipotle, continue to capture the resilient higher-income fast-casual demographic without resorting to margin-crushing discounts.

August will deliver the definitive read on this shifting landscape. Broadline retail earnings will provide forward commentary on back-to-school shopping resilience and exact details on trade-down velocity . Paired with the Commerce Department's mid-August Retail Sales release, the data will clarify exactly how much margin insulation cheaper crude actually buys the U.S. consumer.