February 2026 has closed with a thud for the tech sector, leaving investors to sift through the wreckage of a month where the Nasdaq Composite slid nearly 1% on the final trading day alone. While the broad market snapshot shows a neutral sentiment, the price action tells a more specific story: the "easy phase" of the AI trade is over.

For the past two years, the narrative was simple: buy the chipmakers. But as we enter Year 3 of the boom, the constraint has shifted. We are no longer just waiting for GPUs; we are waiting for the electricity to turn them on. This is the AI Power & Infrastructure Wall, and it is reshaping capital flows from software to hardware and utilities.

The "Power Wall" Reality Check

The selloff in February wasn't just about valuation; it was a recognition of physical limits. The 2024-2025 cycle was defined by a shortage of silicon. The 2026 narrative is defined by a shortage of gigawatts. Interconnection delays for new data centers now exceed three years in many markets, replacing chip supply as the primary hard cap on growth.

This physical bottleneck is creating a bifurcated market. While broad tech softens, companies that solve the energy equation are becoming the new defensive plays.

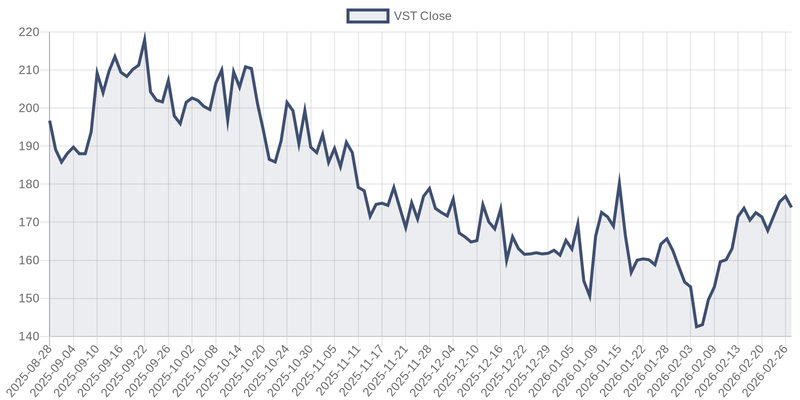

As the chart above shows, independent power producers like Vistra Corp. have become critical to the AI ecosystem. Vistra, along with Eaton Corporation—which provides the switchgear and transformers necessary to upgrade aging grids—represents the "picks and shovels" of this new phase. Scouter AI data highlights these names as the "Power Play" and "Grid Play" respectively, essential for breaking the bottleneck.

Software's ROI Anxiety

While infrastructure stocks grapple with supply constraints, the software layer is suffering from a demand crisis—or at least, a crisis of confidence. The IGV Software Index has been under pressure, down significantly year-to-date, as fears mount that AI is deflationary for traditional SaaS pricing models.

Recent layoffs at fintech firms and "blunt warnings" from CEOs like Jack Dorsey have stoked fears that AI will decimate headcount and, by extension, the seat-based licensing models that software companies rely on. Investors are asking a $600 billion question: *Where is the revenue?* With Hyperscalers projected to spend over half a trillion dollars on Capex this year, the gap between infrastructure spend and software monetization is widening, causing jitters in names like Salesforce and Adobe.

What to Watch: GTC and Earnings

Despite the gloom in software, the infrastructure buildout shows no sign of slowing. The market's attention now turns to two critical upcoming catalysts:

1. NVIDIA GTC (March 2026): All eyes are on NVIDIA for its developer conference. The expectation is not just for faster chips, but for the next-gen "Rubin" or "Ultra" architecture roadmaps that specifically address power efficiency. If NVIDIA can demonstrate that its new silicon delivers more compute per watt, it could alleviate some of the grid pressure.

2. Hyperscaler Earnings (April 2026): The true test of the "ROI Anxiety" thesis will come when Microsoft, Amazon, and Google report Q1 numbers. Investors need confirmation that the $600 billion Capex pace is sustainable. Any sign of deceleration could trigger a broader repricing of the entire AI supply chain.

The Bottom Line: The AI trade isn't dead, but it has become more discerning. The "buy everything" tide has receded, revealing a market that rewards those who own the physical infrastructure—the power, the cooling (Vertiv), and the chips—while punishing those whose business models look vulnerable to the very intelligence they are helping to build. As noted in recent market commentary, the separation between the AI builders and the AI disrupted is likely to widen further in March.