The Information Technology sector enters the first week of June carrying steep valuation premiums, forcing companies to deliver flawless operational updates to defend their multiples. This week's earnings docket spans the entire tech infrastructure stack, from custom AI silicon to global logistics routing. For investors, the setups highlight a tension between structural megatrends—like artificial intelligence and supply chain digitization—and the stark realities of P/E multiple compression.

Here is how Scouter's catalyst models are pricing the risk and reward for three pivotal tech prints landing this week.

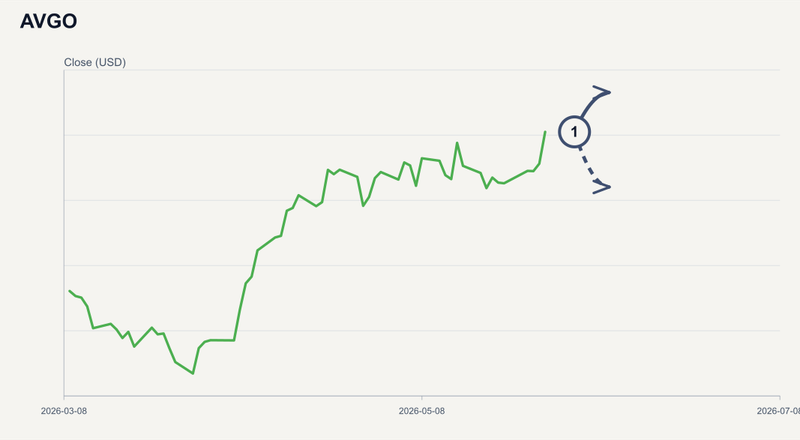

Broadcom's AI Infrastructure Premium

Trading near its 52-week high of $448.90 (closing at $446.77 on Friday, May 29) with its 14-day RSI near 68, AVGO enters its Wednesday, June 3 earnings print priced for perfection. The stock carries an extreme P/E multiple of approximately 84x to 87x, placing enormous pressure on management's ability to demonstrate continued hyper-growth in custom AI accelerator revenue and immediate margin synergies from the VMware integration.

Institutional capital continues to rotate into the hardware layer. Over the weekend, reports highlighted that Stanley Druckenmiller's Duquesne Family Office exited Alphabet entirely in Q1 to load up on AI hardware plays, signaling sustained smart-money confidence in the infrastructure build-out .

The bar for an upside surprise is exceptionally high. However, our empirical data indicates that AI infrastructure suppliers enjoy a 52.9% bull base rate as raw data center demand continues to overpower valuation anxieties. Scouter models an upside target of $471.77—pushing just beyond the standard $22.67 expected move band—if AI revenue explicitly beats expectations. Conversely, if guidance is merely in-line, semiconductors frequently face asymmetric downside digestion, exposing the stock to aggressive multiple compression toward a $411.77 risk floor.

Sprinklr's Search for Reacceleration

While semiconductor names are defending peak multiples, application software providers face a very different setup. CXM approaches its Wednesday earnings print trying to recover from last quarter's dismal 1% full-year revenue growth guidance.

In a bid to reignite growth and capture multimodal customer data, the company recently announced the acquisition of assets of ViralMoment, an AI-powered social video intelligence solution . The market is looking for evidence that these product expansions are translating into sticky enterprise renewals.

Because the previous quarter's cautious guide set the bar remarkably low, the setup carries an asymmetric 0.52 bull probability. Starting from a $5.58 base price, any signs of revenue stabilization or improving customer retention metrics could spark a relief rally beyond typical standard deviations, targeting $5.95. If the weak top-line narrative persists and large enterprise deal cycles continue to elongate, shares risk dragging back down to the $5.15 support level.

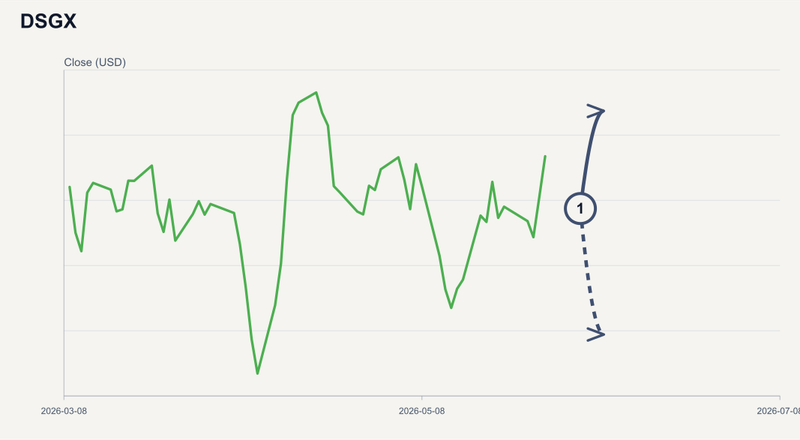

Descartes Faces the Supply Chain Comps

Rounding out the week, DSGX reports on Wednesday, June 3 . The global logistics and routing software provider must prove it can sustain mid-teens revenue growth against exceptionally tough year-over-year comparables.

Like many defensive Application Software names that benefited from global trade disruptions over the last two years, Descartes is grappling with valuation friction, currently trading with a 39x P/E overhang.

With the stock having recently retraced from its highs to a $73.77 base, Scouter's models account for a wider-than-normal volatility band. Robust logistics intelligence demand provides a supportive tailwind that could drive a recovery to the $76.00 target if Billed B2B Volumes impress. However, any unmitigated operational cost pressures or volume deceleration could trigger a slide toward the $65.00 risk floor as the market reprices the premium multiple.