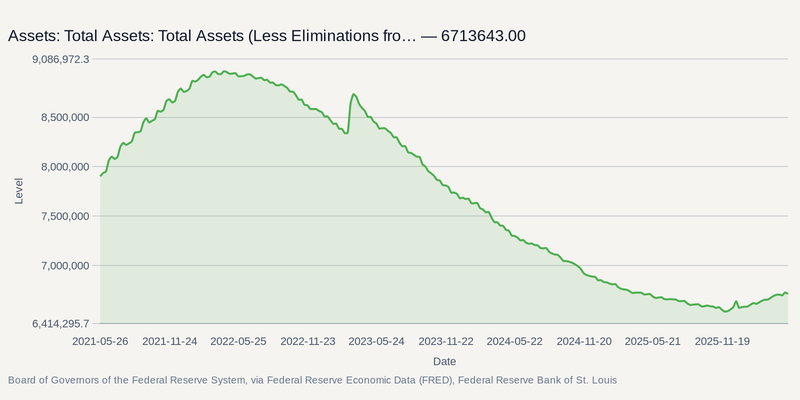

While equity markets spend their sessions obsessing over the precise terminal rate, a far more consequential structural shift is brewing deep within the U.S. financial system. Newly sworn-in Federal Reserve Chair Kevin Warsh has telegraphed a profound "regime change" for the central bank, one that fundamentally rethinks how the institution manages the day-to-day plumbing of the economy. His proposed agenda aims to shift the Fed away from using its $6.7 trillion balance sheet as a daily tool for influencing financial conditions, reserving it instead strictly for periods of severe market dysfunction.

For the financial sector, this potential withdrawal of a persistent liquidity backstop changes the math for everything from daily treasury operations to merger strategies. If the Fed moves away from backstopping the daily mechanics of the market, balance sheet scale and deposit stability become the ultimate premium assets. This dynamic is helping fuel the Banking Sector Rebound & Consolidation trend, forcing regional and super-regional players to consider merging or risk being left vulnerable to liquidity shocks.

Rewiring the Financial Plumbing

The debate over the Fed's footprint is highly technical, but the transmission mechanism to equity valuations is immediate. Since the 2008 crisis, the Fed's balance sheet ballooned, sitting at roughly 21% of the U.S. economy today. Unwinding this "bloated" position, as newly appointed Fed Chair Kevin Warsh described it in a November 2025 op-ed, means Treasury yields, mortgage rates, and net interest margins (NIM) will trade more heavily on raw market fundamentals rather than central bank intervention.

Regulators are already preparing the groundwork for this new era of self-reliance, having just signed off on the "living wills" submitted by the nation's largest banks detailing how they could be safely unwound in bankruptcy. With the regulatory framework firming up, the pressure is on regional players to adapt. Institutions like PB (Prosperity Bancshares) are fast-tracking their strategic acquisition pipelines, while PNC continues to consolidate market share following its buyout of FirstBank Holding Company .

Global Dealmaking and Strategic Outposts

Beyond domestic M&A, the top-tier global banks are flexing their capital advantages to capture specialized growth ahead of the Fed's pivot. The industry's definitive bellwether, JPM, alongside core holding BAC, are positioning for a robust recovery in investment banking flows.

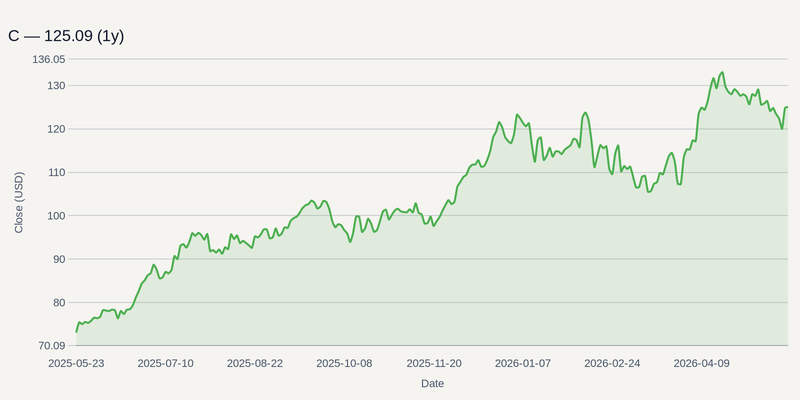

Meanwhile, turnaround plays are getting aggressive. C (Citigroup) is actively boosting its investment banking teams in Japan and China, deploying targeted senior hires to close coverage gaps in Japan's technology, media, and telecommunications sector, while focusing on "new-age" and "high-growth" companies in China .

Yield Curve Friction and Regulatory Headwinds

The transition to a smaller Fed footprint is not without structural friction. Elevated interest rates continue to expose vulnerabilities beneath the surface of the banking rebound. A major U.S. investment bank is still grappling with soured legacy deals and underperforming alternative investments, particularly tied to a debt-heavy corporate roll-up financed before the rate-hike cycle .

On the compliance front, the Trump administration issued an executive order this week requiring increased scrutiny of non-citizens' banking activities, adding a new layer of operational overhead for compliance departments . Though less severe than early proposals requiring banks to actively collect citizenship data, it highlights the unpredictable regulatory surface area banks must navigate while simultaneously managing their integration costs.

As the Fed prepares to step back from the plumbing, investors will get a clear look at who is built for the new regime during the Q2 2026 earnings season beginning in mid-July. Those prints will serve as critical barometers for investment banking fee recovery and, more importantly, whether these newly consolidated regional balance sheets can protect their net interest margins without a central bank safety net.