Kevin Warsh is being discussed as a possible future Federal Reserve chair at a perilous juncture. If confirmed by the Senate, he would face political pressure from the White House to lower borrowing costs just as wholesale inflation shows renewed strength.

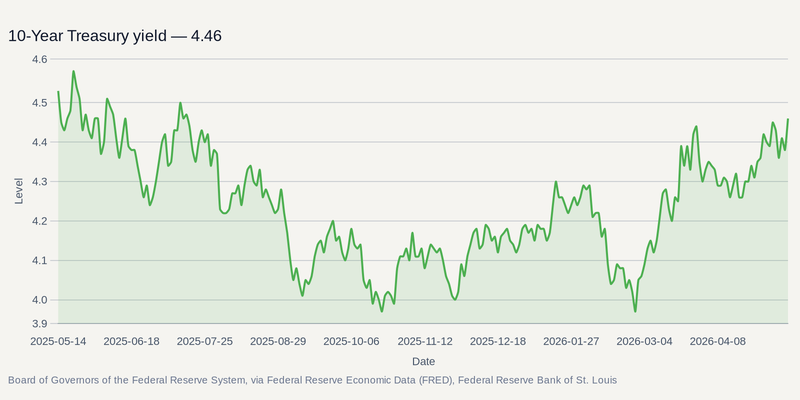

The April Producer Price Index (PPI) surged 1.4% month over month, according to the Bureau of Labor Statistics . The report pointed to broad price pressures, including higher energy costs, while Treasury yields rose as markets digested the inflation data.

Where the trajectory of the 10-year yield reflects the market's inflation anxieties, the underlying tension at the central bank has sparked a broader Central Bank Independence Erosion Play. Warsh has previously criticized the Fed's 2020 easy-money policies, and any new chair would likely face intense political pressure to lower rates heading into an election cycle.

Navigating the Institutional Collision

The immediate risk for markets is not just hot inflation—with April’s Producer Price Index (PPI) jumping to 6% year-over-year—but the fracturing of the consensus-driven Federal Open Market Committee. While the administration publicly demands a dovish pivot to lower rates, internal momentum is skewing hawkish. Boston Fed President Susan Collins (a non-voting member in 2026) has already flagged the potential need for rate *hikes* if the energy-driven inflation broadening into core data—which hit 5.2% at the wholesale level—is not contained.

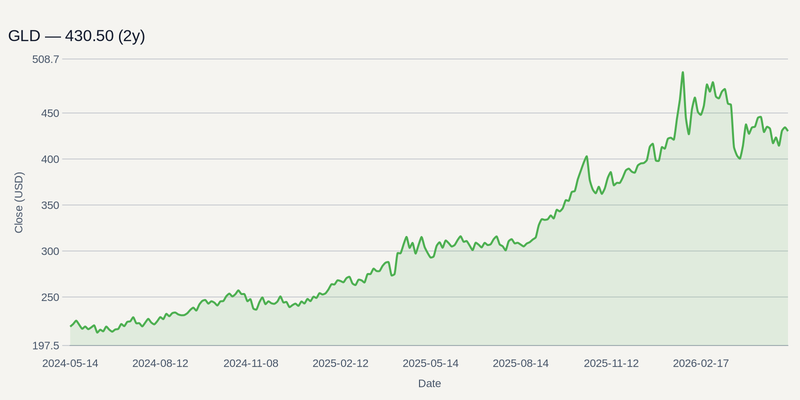

This friction—between political desires for liquidity and the economic necessity of restriction—changes how capital prices institutional credibility. When fiat governance faces perceived political subjugation, capital historically flows into sovereign safe havens. It is this exact dynamic that is driving a structural re-rating across Materials and specifically the Gold complex.

The Hard Asset Transmission

Investors are increasingly treating precious metals not merely as an inflation hedge, but as a hedge against perceived monetary-policy risk. Direct exposure via vehicles like the SPDR Gold Shares has drawn interest ahead of the June FOMC meeting.

Beyond the physical proxy, the setup for precious-metals miners can improve when gold prices outpace energy and other input costs. Newmont Corporation is among the large-cap producers that could benefit if elevated bullion prices persist.

The main risk to this hard-asset rotation would be a sharp rise in real rates, which could pressure gold and other non-yielding assets if the Fed keeps policy tighter for longer. If rates rise enough to restore the dollar’s yield advantage, gold could face a temporary liquidity hit.

Volatility as a Feature

Yet, even in a scenario where the Fed holds the line, the sheer volume of uncertainty surrounding the committee's forward path is tradable. The clash over institutional autonomy virtually guarantees heightened rate volatility through the summer.

This erratic rate-expectation environment serves as a direct catalyst for financial infrastructure plays like CME Group Inc.. As regional banks, asset managers, and corporate treasuries scramble to hedge against sudden shifts in both the yield curve and commodity inputs, derivative exchanges stand to capture the elevated clearing volumes. Until the supply chain bottlenecks in Hormuz clear or the political heat on the Fed dissipates, volatility and hard assets remain the market's preferred shock absorbers.