The broader software sector is undergoing a violent bifurcation. Since early 2025, median revenue multiples for software firms have compressed from above 7x to below 5x . But beneath the surface of this valuation reckoning, a distinct rotation is underway: capital is abandoning undifferentiated seat-based models and flowing into verticalized, AI-monetized platforms.

Investors are forcing a shift from theoretical large language model capability to tangible operational efficiency. As venture capital and private equity pivot toward hardware and infrastructure, legacy software providers face a potential funding freeze—what industry observers are dubbing a "SaaSpocalypse" . Yet, specialized enterprise Software-as-a-Service (SaaS)) deployments are seeing an early bullish inflection, driven by organizations finally integrating generative workflow features into daily execution.

Verticalization Reaches Main Street

The artificial intelligence narrative is migrating from multi-billion dollar data centers to the physical economy. The deployment layer is expanding aggressively—AI agents are now routinely deployed to scrape spreadsheets for local bakeries, while retail heavyweights like Walmart and Sephora embed algorithmic logic directly into the online shopping cart experience.

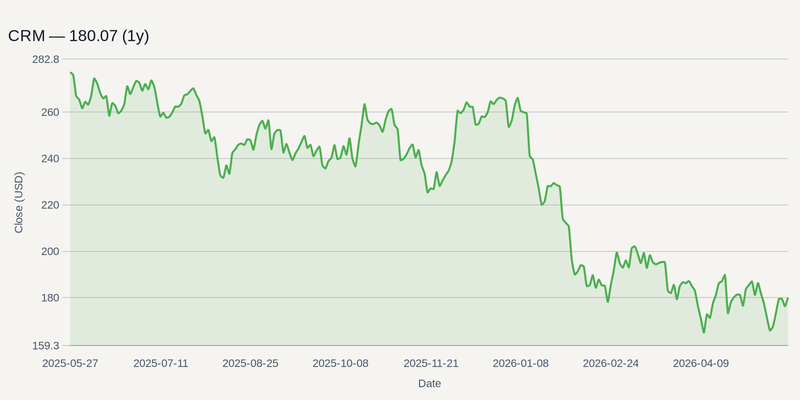

This shift toward domain-specific utility is expected to drive the vertical software market from roughly $133.5 billion in 2025 to $194.0 billion by 2029 . As hardware delivery converges with software monetization roadmaps, companies like CRM and NOW are racing to prove that their AI assistant ecosystems can drive measurable cost efficiencies for clients, rather than just adding expensive licensing tiers.

The Consolidation Floor

For the vast middle-tier of the SaaS market that lacks specialized AI integration, the path forward is looking increasingly binary: innovate or be acquired. The reckoning has spilled into private equity, where firms are restructuring portfolios to account for the evaporation of the "growth at all costs" premium .

However, this pressure is establishing a structural valuation floor via M&A. Strategic acquisitions within Information Technology are maintaining a high pace as ecosystem providers buy up niche tools to build out comprehensive, sticky platforms. The inherent network effects of these larger ecosystems create formidable barriers to entry, insulating the consolidators from the broader multiple compression .

Securing the Agentic Enterprise

If the next phase of enterprise software relies on autonomous agents executing workflows and scraping proprietary data, the attack surface expands exponentially. This dynamic explains why cybersecurity names have shown relative resilience compared to the broader sector's multiple contraction.

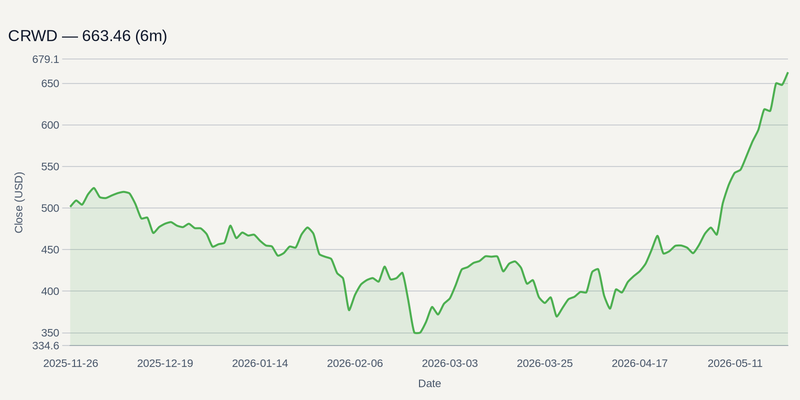

Vendors such as CRWD, ZS, and PANW continue to command premium valuations, directly benefiting from sustained enterprise investments mandated to protect these newly enabled AI workflows . Zero-trust architecture is no longer an optional IT upgrade; it is a prerequisite for deploying enterprise AI safely.

The Q1 Earnings Litmus Test

The durability of this rotation will be tested immediately. A heavy slate of bellwether earnings kicks off tomorrow with Zscaler, followed by Salesforce testing its Agentforce monetization narrative on Wednesday, May 27. Palo Alto Networks and CrowdStrike take the stage on June 2 and June 3, respectively.

Markets are no longer rewarding SaaS providers simply for announcing AI integrations. This earnings window will require explicit commentary on how domain-specific AI is expanding net revenue retention and offsetting the traditional seat-license decay. Providers that can demonstrate this pipeline conversion are poised to capture the capital fleeing the legacy software stack.