For the last six weeks, global capital markets have been suffocating under the threat of a severe stagflationary shock. That pressure was suddenly released late Tuesday when a two-week U.S.-Iran ceasefire was announced, opening a pathway to unblock the Strait of Hormuz. The macroeconomic math shifted instantly: benchmark U.S. crude plunged nearly 16% to $94.52 a barrel, averting an acute energy crisis and sparking a fierce, immediate risk-on rally across equities and bonds.

But beyond the euphoric premarket surges in the S&P 500 and Nasdaq, the most critical shift is happening within the Federal Reserve's policy outlook. Prior to the ceasefire, the central bank was trapped. Minutes from the Fed’s March meeting, released Wednesday, revealed policymakers were highly concerned about the geopolitical conflict, warning that substantially higher oil prices could force them to remain hawkish to fight imported inflation—even at the cost of household purchasing power.

Now, the sudden deflationary relief at the gas pump has shifted the narrative from "higher for longer" back to an imminent Macro pivot. Institutional sentiment rapidly abandoned stagflation fears, moving heavily into bonds as Treasury yields plummeted. According to CME Group's FedWatch Tool, market pricing for a Fed rate cut by December 2026 spiked overnight from a mere 14% to 43%.

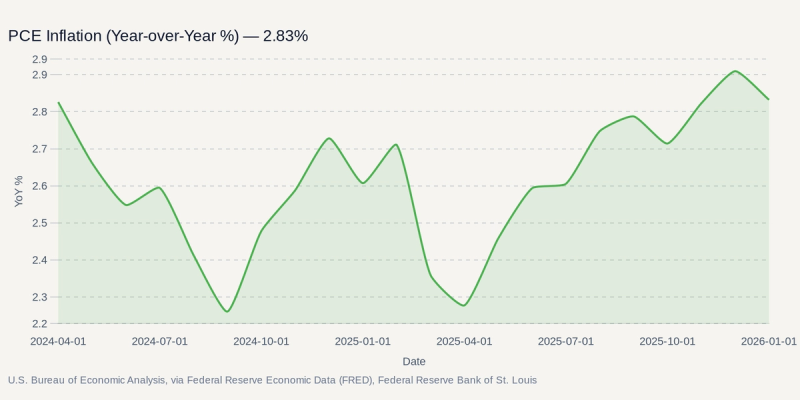

As the chart below illustrates, inflation has been a stubborn adversary for central bankers over the last two years, forcing them to hold policy at highly restrictive levels.

This rapid repricing comes at a time when the Fed's institutional independence is under a microscope. Chair Jerome Powell is facing immense political pressure, including an ongoing legal battle over subpoenas from U.S. Attorney Jeanine Pirro and the administration's vocal push to swiftly confirm Kevin Warsh as his eventual replacement. In this highly charged environment, a sustained drop in energy prices provides the Fed with the exact macroeconomic cover it needs to justify rate cuts and appease both market and political demands.

However, the dominant narrative carries a significant blind spot. This ceasefire is inherently fragile—a two-week pact contingent on complex Islamabad talks set to expire around April 22. While crude oil has retreated from its peak, $94.52 per barrel is still historically elevated, and global energy supply chains will require months to fully normalize. Furthermore, underlying core inflation, particularly in shelter and services, remains notoriously sticky. If the diplomatic window closes without a permanent resolution, the energy shock will reignite, instantly trapping a Fed that just signaled a willingness to be "nimble."

For investors, the immediate focus is on the upcoming March Consumer Price Index (CPI) release on April 10, which will dictate whether this dovish momentum holds into the critical May 6 FOMC meeting. In the interim, capital flows are heavily favoring Financials and fixed income. Long-duration bonds via the TLT (iShares 20+ Year Treasury Bond ETF) offer a direct play on falling long-term yields as markets price out further hikes.

Meanwhile, the extreme macro volatility and massive institutional hedging volume are creating distinct tailwinds within Capital Markets. Exchanges like CME are positioned to profit from surging derivative volumes, while asset managers and investment banks such as BLK and GS stand to capture the heavy capital inflows and revived deal-making activity born from this sudden return to a risk-on environment.