The global energy market is undergoing a structural realignment that is fundamentally altering capital flows across the broader economy. Following the United Arab Emirates’ departure from OPEC on May 1, the cartel’s grip on global pricing has fractured just as the U.S.-Israel conflict with Iran severely constrains the Strait of Hormuz. This dual supply shock has cemented structurally elevated crude prices, rapidly accelerating a profound Upstream E&P Supercycle for domestic operators.

While broad indices wobbled today—with the Dow sliding more than 500 points as inflation fears pulled capital out of equities and into defensive havens—the underlying rotation is clear. High oil prices are acting as a wrecking ball for high-multiple growth stocks but serving as an unprecedented cash-generation engine for pure-play exploration and production names.

The UAE Pivot and Cartel Capitulation

The UAE's production ambitions underscore the growing tension inside OPEC, but it has not exited the group. Long frustrated by playing second fiddle to Saudi Arabia, the UAE has been pushing to expand its upstream capacity, with plans that have at times pointed to about 5 million barrels a day by the late 2020s, up from roughly 3.3 million barrels a day.

Rather than an immediate price collapse, Middle East geopolitical risk has helped keep a risk premium in crude prices, while the eventual unraveling of OPEC quotas would likely shift the battle toward market share. For investors, the takeaway is twofold: the geopolitical risk premium remains supported in spot prices, while any loosening of OPEC discipline could intensify longer-term competition among producers.

Yield Spikes Threaten the AI Multiples

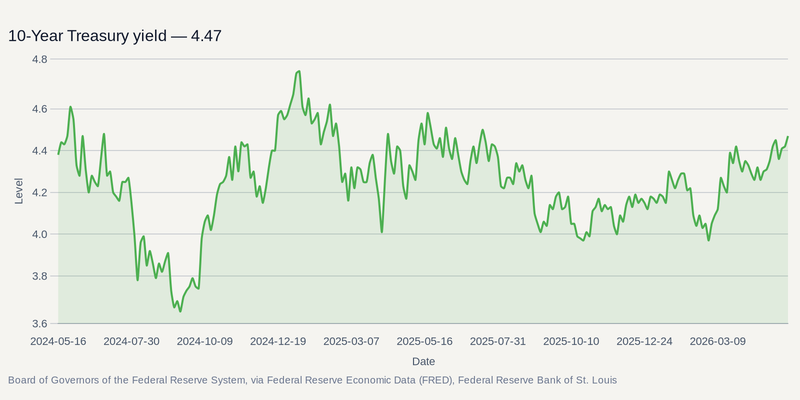

The ripple effects of this energy shock are heavily dictating broader market structure. As crude holds at elevated levels, the prospect of sticky inflation has forced bond markets to price in a “higher for longer” reality, sending the 10-year Treasury yield to its highest level since May 2025.

This dynamic triggered a massive rotation away from the highest-duration growth pockets today. Semiconductors and artificial intelligence supply-chain names faced heavy selling pressure as multiples compressed in the face of rising discount rates. The trade logic here is mechanical: when energy keeps inflation expectations elevated, capital retreats from high-flying tech sectors and seeks refuge in either long-duration Treasury bonds on recession-risk hedging, or highly profitable commodity operators.

Peak Cash Flow and the M&A Boom

For the U.S. upstream sector, the current price regime is transformative. Pure-play operators are highly leveraged to underlying commodity prices; even with recent price volatility following the UAE’s formal exit from OPEC on May 1, 2026, many operators continue to generate significant free cash flow.

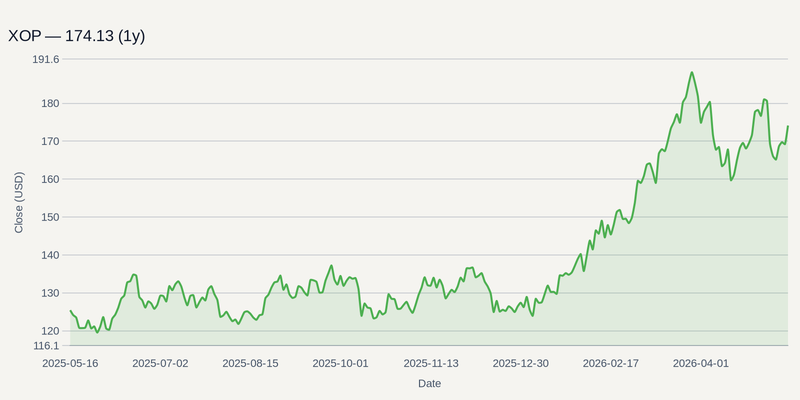

The capital surplus is entirely reshaping corporate balance sheets. Instead of the undisciplined capacity expansion seen in previous cycles, operators are prioritizing aggressive debt reduction, massive shareholder yields, and a historic wave of industry consolidation. Momentum in the SPDR S&P Oil & Gas Exploration & Production ETF has surged this year—up more than 40% year-to-date as of early May—as retail and institutional investors flock to exploration names as tangible inflation hedges.

Corporate confidence is echoing this sentiment. The recently completed $25 billion mega-merger between Devon Energy Corp and Coterra Energy highlights the premium placed on scaled, efficient operations. Other heavily leveraged names like Occidental Petroleum are utilizing the crude windfall to execute aggressive debt-reduction theses, having successfully lowered principal debt to approximately $13.3 billion as of May 2026. Meanwhile, large-cap stalwarts like ConocoPhillips are positioned to return immense capital to shareholders, maintaining a target to return 45% of cash from operations in 2026.

Supply Wildcards: The June Catalysts

The primary risk to this bullish upstream thesis is a sudden influx of spare capacity or a sharp geopolitical off-ramp. If the Middle East conflict sees a rapid diplomatic de-escalation, the risk premium embedded in crude could fade quickly. Furthermore, if more OPEC+ members abandon quotas and choose to boost output, the resulting supply glut would quickly challenge U.S. operator margins.

The durability of this supercycle will be tested in the coming weeks. The 41st OPEC and non-OPEC Ministerial Meeting, scheduled for June 7, is expected to clarify how Saudi Arabia intends to manage the cartel's remaining credibility, followed closely by the U.S. Energy Information Administration's Short-Term Energy Outlook, expected around June 9. Until the physical chokepoints clear, domestic E&P names remain one of the few insulated harbors in an increasingly inflation-rattled market.