Broad equity indices are catching a strong bid today, with the S&P 500 pushing 1.48% higher in trading. But beneath the surface of the resilient U.S. consumer narrative, retail performance remains uneven: higher-income shoppers have generally continued to spend on services and premium goods, while lower-income households remain more sensitive to inflation, borrowing costs, and energy prices.

Some Wall Street economists have argued that higher gasoline prices can blunt part of the seasonal boost from early-year tax refunds. This K-shaped backdrop can alter the risk-reward profile for Consumer Discretionary equities as we move deeper into the second quarter.

Regressive Taxation at the Pump

Recent geopolitical tensions in the Middle East have helped push U.S. gasoline prices higher, acting as a direct hit to discretionary spending. Unlike broader inflation metrics, fuel costs can change household budgets quickly.

Recent data highlights how stark this divide can be. According to the New York Fed, lower-income households cut driving more than higher-income households during an energy-price spike, but still saw larger increases in nominal spending at the pump because prices rose so sharply . In other words: they drove less, but still paid more.

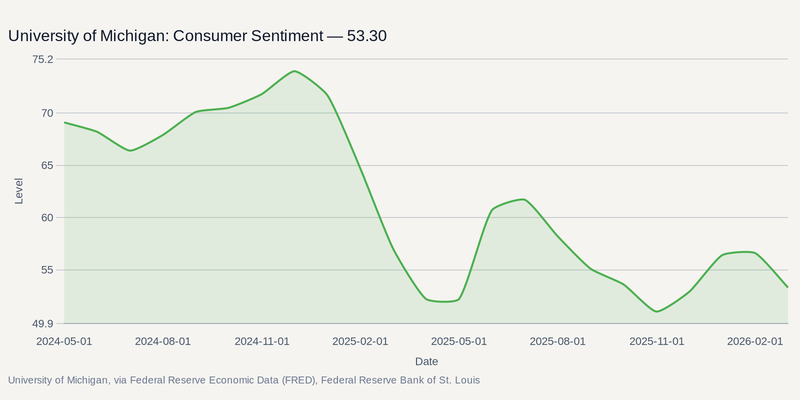

That dynamic also feeds into broader sentiment and inflation-expectations measures. Near-term inflation expectations among lower-income households have tended to run higher, and sentiment has been weaker at the bottom of the income distribution. We’ll get another read on that gap when the preliminary University of Michigan Consumer Sentiment report is released on May 8.

When Aggregate Data Masks the Cliff

For institutional investors, the risk is that aggregate retail sales figures can mask localized weakness. Sector-wide earnings beats in early 2026 have been helped by higher-income consumers. Spending on travel, experiences, and premium goods can look healthy at the macro level, but it may obscure softer volumes at the lower end.

Furthermore, the temporary support from tax refunds and seasonal promotional cycles is starting to fade. Once that liquidity boost diminishes, retailers exposed to lower- and middle-income households may have less buffer against still-elevated fuel and energy costs.

Trade-Down Beneficiaries and Defensive Moats

This environment requires a tactical rotation within retail, favoring companies structured to absorb margin pressure or explicitly designed to capture trade-down volume.

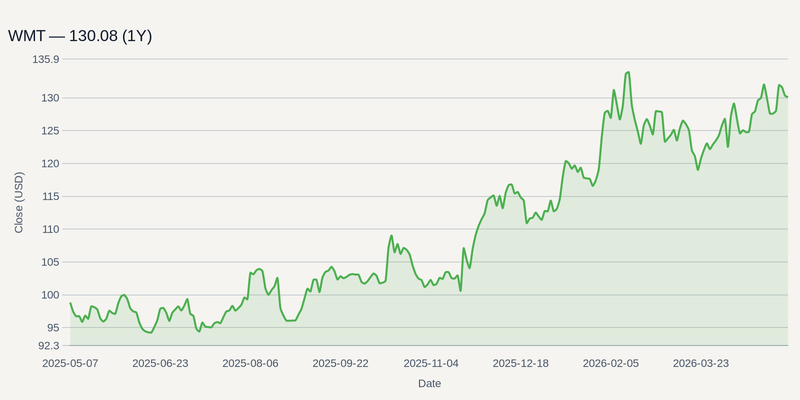

Walmart Inc. remains the primary vehicle for capturing the middle-class trade-down effect. As household budgets tighten, groceries and essential consumables become the anchor for foot traffic, allowing mega-cap discounters to grab market share from traditional grocers and regional department stores.

Similarly, off-price models like The TJX Companies, Inc. historically thrive in this exact regime, operating as a primary destination for middle-income shoppers hunting for bargains. On the other end of the spectrum, Costco Wholesale Corporation offers significant defensive insulation; its membership subscription model and higher-income demographic base shield its core cash flows from the immediate shocks of fuel price volatility.

Even Amazon.com, Inc. warrants attention here. While not immune to a broad consumer slowdown, its physical retail weakness is heavily offset by its entrenched e-commerce dominance and recurring cloud revenue, making it a lower-beta play on the consumer cycle compared to mall-based physical retail.

The Path to Reversion

The primary threat to this defensive thesis lies in the energy markets. If geopolitical premiums evaporate and crude oil prices break aggressively lower, the pressure on jet fuel and gasoline would reverse. A rapid return to sub-$3.50 gasoline would act as an immediate, un-modeled stimulus check for the sub-$40,000 income bracket. Under that scenario, the extreme K-shaped divergence would flatten, and heavily shorted, high-beta discretionary names would likely catch a violent squeeze.

However, until energy markets signal a structural breakdown in pricing, the base case remains cautious. With major retail earnings from Walmart and Target arriving later this month, forward guidance will be the ultimate tell. Management commentary dissecting ticket size versus foot traffic will confirm just how deeply the pump has cut into the consumer's wallet.