The Port of Los Angeles quietly hit a June cargo record this week, and the U.S. industrial construction pipeline just spiked 18% year-over-year in the second quarter. This isn't a repeat of the pandemic-era scramble for consumer electronics. What we are watching is a massive, capital-intensive rewiring of how physical goods move—a slower, more permanent rebuild of warehouse, port, and inland-distribution capacity centered on reshoring and inventory resilience. (In plain English: more boxes need more places to sit, and they need to get there faster.)

The new physical bottleneck

Shippers are aggressively front-loading ocean freight to get ahead of the looming July 24 expiration of Section 122 tariffs and the transition to proposed Section 301 duties . But downstream, the Industrials ecosystem is realizing that supply chains are no longer just cost centers; they are structural bottlenecks with immense pricing power. Downstream movement has stayed remarkably robust, allowing operators to command a premium for warehouse availability and strategic facility access as capacity contracts .

Leaner inventory models and the ongoing friction of tariff volatility increasingly dictate real estate demand in the warehousing sector . Companies are paying up to secure their throughput.

Margin expansion through scarcity

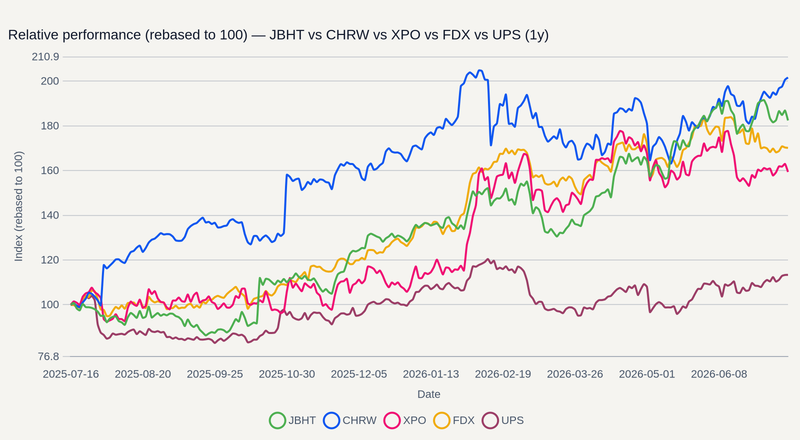

The mechanics here are straightforward: tighter market capacity plus rising shipping rates equals outsized margin expansion for the players who control the logistics grid. J.B. Hunt Transport Services validated this thesis today, July 15, delivering a blowout quarter with a 45% surge in earnings per share on record intermodal volumes (and its long-suffering brokerage unit even turned a profit for the first time in 14 quarters, proving that patience occasionally pays off).

Shippers, who enjoyed the upper hand over the past three years of normalizing supply lines, are suddenly facing drastically tougher market conditions . To maintain that leverage, freight brokers and carriers are wielding ruthless cost discipline to convert volume growth directly into free cash flow. For diligence, asset-light brokerages like C.H. Robinson offer a compelling case study: they are built to capture upside from tightening truckload capacity without carrying heavy fleet capital on their own balance sheets.

The logistics utility race

The biggest operators aren't just moving freight; they are transforming into standalone supply chain utilities. Amazon is officially decoupling its fulfillment network to launch Amazon Supply Chain Services, shifting from a retail marketplace engine to an AWS-style utility for third-party logistics . Meanwhile, structural consolidation is accelerating. FedEx is offloading its contract logistics unit to CMA CGM in a $1.4 billion deal (which, in a classic corporate circle of life, is the exact same price FedEx paid to buy the business a decade ago) expected to close later this year .

But building a global utility isn't cheap, and the macro backdrop is unforgiving. Persistent fuel drags and Middle East maritime bottlenecks are already eating into margins. If retail demand stumbles in the back half of 2026, shippers will retrench—collapsing the exact volumes needed to fund these capital-heavy infrastructure bets.

Pricing the capacity constraint

Scouter's Integrated Freight Margin Expansion data helps you assess how these physical bottlenecks flow through to equity valuations. When United Parcel Service reports its second-quarter financials on July 28, the market will treat the print as a critical bellwether for global parcel and B2B healthcare logistics demand .

The edge in this cycle belongs to the names that don't just participate in the volume surge, but own the chokepoints. Pure-play less-than-truckload (LTL) carriers like XPO are soaking up spillover volume as truckload constraints force shippers to hunt for alternative domestic routing. The freight market isn't merely normalizing—it is being permanently repriced.