The U.S.-Iran ceasefire initially uncorked a wave of relief across global capital markets, sending broad proxies like SPY into a multi-week risk-on sprint. But beneath the surface, the foundation of this rally is fracturing. Investors are eagerly pricing in a return to lower interest rates, assuming the fragile pause in hostilities will instantly reverse stagflationary pressures and clear the runway for a dovish Post-Ceasefire Fed Pivot. Yet, a closer look at the data suggests this premature celebration is on a collision course with sticky core prices and a deeply hostile bond market.

The Ceasefire Illusion and Sticky Core Prices

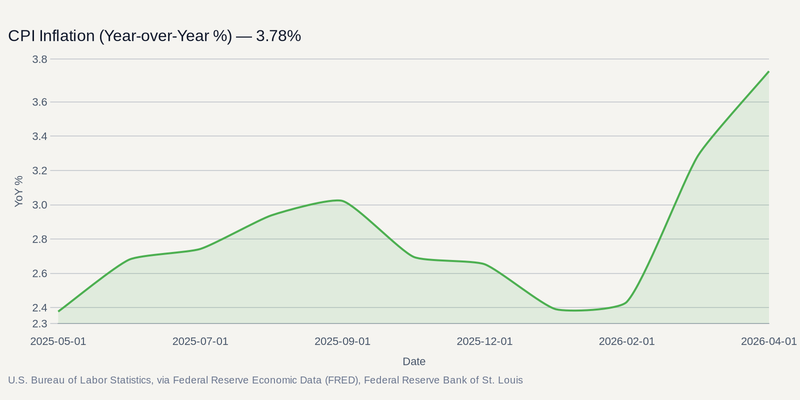

While oil prices have slipped from their wartime peaks, the broader economic shock may extend beyond energy markets. Central bankers are typically reluctant to adjust long-term policy based on temporary commodity volatility, and recent data has pointed to still-sticky inflation pressures during the weeks of the conflict .

Federal Reserve officials have said they are not in a rush to cut borrowing costs, and some reporting has said policymakers have even discussed the possibility of higher rates if price pressures prove persistent . The next monthly inflation release, covering May data, is due in mid-June, and it will help show whether the recent disinflation trend has been interrupted. A durable resolution would likely require more than a temporary pause in fighting, and some analysts have warned that fiscal positions globally could deteriorate further as debt-service costs stay elevated .

Warsh's Conundrum and the Return of Bond Vigilantes

This fundamental reality collides with intense political pressure if President Trump were to install Kevin Warsh as Fed Chair, with markets already focused on whether the next Fed chief would face demands for faster rate cuts while managing a Treasury market that is pushing back against further easing.

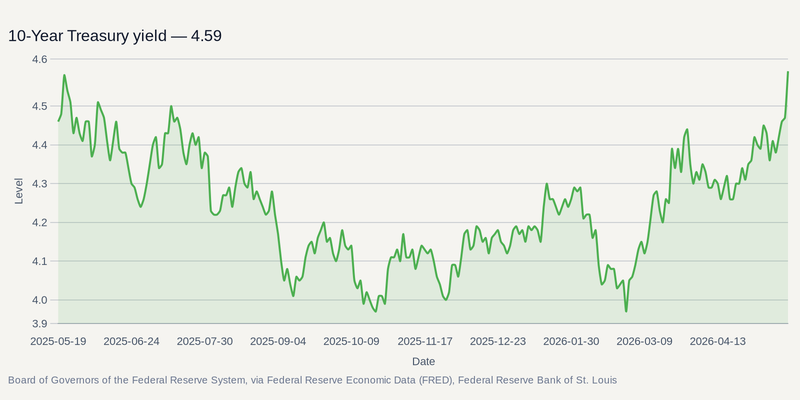

Yields are effectively doing the central bank's tightening work for them. The 10-year Treasury yield has recently been trading in the mid-4% range, punishing duration-sensitive tech names and raising corporate borrowing costs. Some analysts, including Ed Yardeni, have argued that instead of delivering cuts, the central bank may eventually need to tighten policy to satisfy these "bond vigilantes" and avoid losing control over the long end of the curve.

For traders holding heavy exposure to long-duration bonds through vehicles like TLT, this represents a severe mispricing. The market has attempted to look through the inflation data, but current pricing still leaves open the possibility of higher rates later this year, complicating the outlook for growth equities.

Capitalizing on Rate Uncertainty in Financials

If the base case shifts from a smooth dovish glide path to a volatile, higher-for-longer regime managed by a politically besieged Fed—now under the newly installed leadership of Chair Kevin Warsh as of May 15—the transmission mechanism naturally favors the Financials sector. Massive swings in yield curves and macro hedging directly feed capital markets activity.

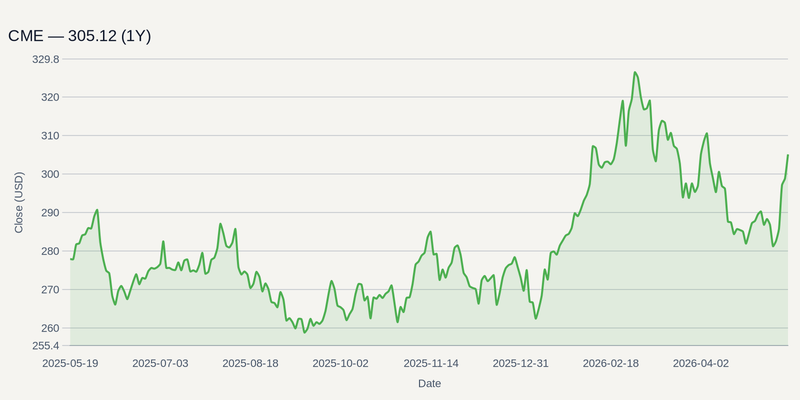

Institutions like JPM and GS serve as primary bellwethers for this environment, positioned to absorb the loan growth repricing and a resurgent investment banking pipeline generated by corporate repositioning. Furthermore, exchange operators like CME stand out as direct beneficiaries of the record interest rate hedging volumes—which reached an average daily high of 36.2 million contracts in Q1 2026—tied to shifting FOMC expectations. The April 10 ceasefire in the Iran conflict may have averted an immediate crude oil supply shock, but for the new Fed leadership, the war on inflation is far from over as price pressures remain sticky.