The EV & Autonomous Mobility Transition is actively fracturing into a two-tiered market. On one side, pure-play vehicle manufacturers are contending with stagnant consumer adoption and shifting preferences toward hybrids. On the other, the underlying component suppliers and infrastructure builders are aggressively capturing the upside of a profound structural shift. Despite the near-term friction in dealership lots, the broader sector is quietly organizing itself to chase an estimated $10 trillion total addressable market for autonomous driving applications .

Rather than viewing the electric vehicle transition as a monolithic auto trade, capital is rotating toward the critical bottlenecks of the ecosystem: battery efficiency, charging speeds, and the computing power required to bridge the gap between human operation and fully autonomous fleets.

Silicon Carbide and the Hardware Fix

The most immediate roadblock to mass EV adoption has been range anxiety and charging downtime. Automakers cannot simply software-update their way out of battery chemistry limitations, which has turned advanced power electronics into a massive profit pool.

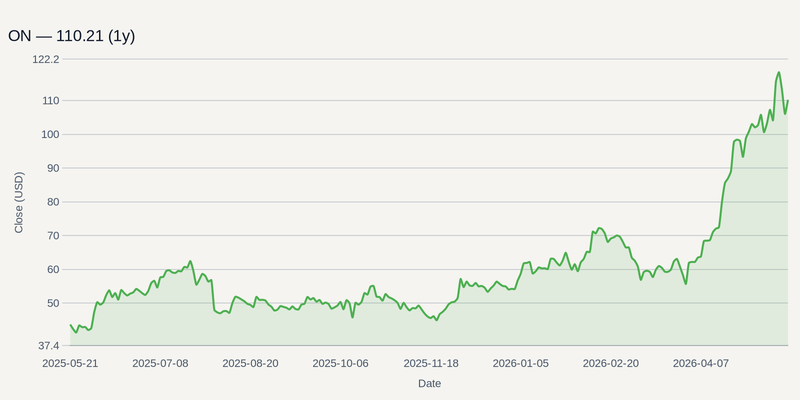

Semiconductor companies are stepping into this void. ON has become a critical supplier in this space, leveraging silicon carbide MOSFETs that can effectively increase an electric vehicle's range by 7 percent while simultaneously cutting charging times by half .

When components materially alter the consumer experience—and the unit economics for automakers—the suppliers command premium multiples. Similarly, STM continues to leverage its automotive chip positioning to bridge the gap between traditional hardware and next-generation low earth orbit (LEO) satellite connectivity. As STM hosts dedicated investor presentations through the spring—including its May webcast detailing its LEO satellite roadmap—the market is pricing these names less like traditional automotive suppliers and more like advanced infrastructure plays.

The Battery Infrastructure Land Grab

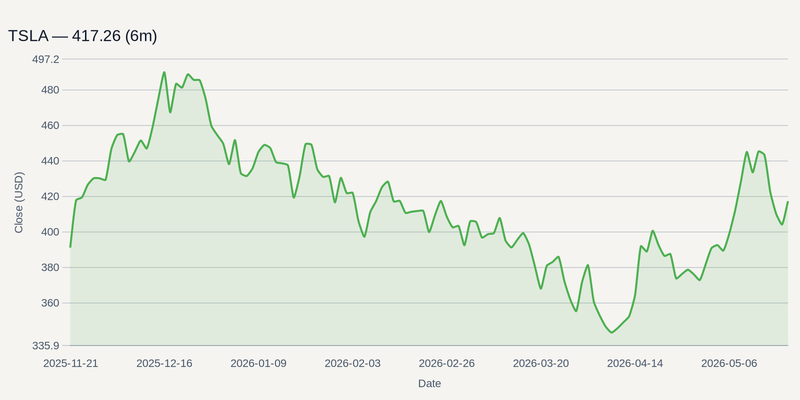

While legacy OEMs scale back pure-EV targets in favor of hybrid stopgaps, the sector's bellwether is doubling down on hard industrial capacity. TSLA is actively expanding its battery cell production footprint, recently committing an additional $250 million to boost capacity targets at its plant outside Berlin .

This capital allocation underscores a critical realization: the winners of the mobility transition will be those who control the underlying energy networks, not just the sheet metal. Broadening EV adoption requires massive enhancements to charging infrastructure and strategic industry partnerships . The focus on regional build-outs is also driving global capital flows, heavily featured at upcoming industry summits like the MOVE Middle East conference, which is drawing mobility leaders to establish future electrification targets in fossil-fuel-heavy regions.

Pure-Play Automakers Hit a Wall

The contrast between infrastructure momentum and pure-play auto manufacturing remains stark. Companies like RIVN and LCID are navigating a severe demand slowdown. These pure-play electric truck and luxury manufacturers are forced to manage cash burn while attempting to stimulate stagnant sales through new model introductions.

For investors, the near-term headwind is clear: the cost of manufacturing complex vehicles in a high-rate, cautious-consumer environment is punishing pure-play automakers. However, the secular tailwinds for reduced emissions and advanced autonomous road safety remain intact. The actionable edge lies in moving up the supply chain—targeting the advanced semiconductors and battery scaling operations that power the fleet, regardless of which automaker's badge is on the steering wheel.