The core message in Consumer Spending Resilience With Emerging Cracks is not that the consumer has rolled over. It is that spending is still happening, but the mix is getting narrower: staples, value, and lower-ticket purchases are holding up better than higher-ticket discretionary categories. That is the kind of split that matters for the next several quarters because it changes who can protect traffic, who can defend margin, and who gets punished first when wallets tighten.

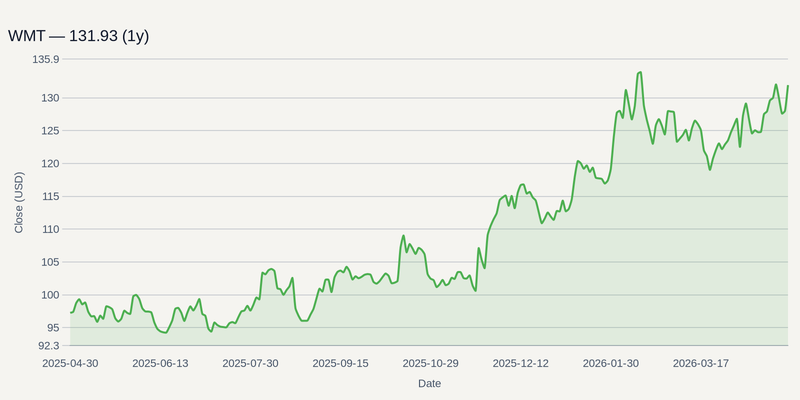

For investors, that usually favors the franchises with either clear trade-down capture or everyday-need exposure. Walmart can keep pulling in value-conscious households, McDonald’s benefits from lower-ticket meal occasions, and Ross Stores can gain from consumers hunting discounts. Amazon sits in a different lane: it can still benefit from resilient online demand, but also from the broadest assortment and the ability to absorb smaller basket sizes without depending on one category. In other words, the winners are increasingly the names that can serve a cautious shopper without forcing a premium decision.

The pressure is showing up where budgets are most sensitive to rates and real income. Elevated borrowing costs raise the hurdle for furniture, home improvement, and other big-ticket purchases, while slower wage growth and lower savings make lower-income households more likely to trade down or delay. That is why the signal is not just about one weak retail print; it is about the duration of the slowdown in higher-ASP categories and whether management teams start talking more about conversion, trade-down, and selective traffic rather than broad demand growth. Home Depot sits directly in that pressure zone: if housing-related spending remains intact, the stock can work, but it is more exposed than a value grocer or quick-service chain if consumer budgets keep softening.

Saks Global has said it is cutting about 16% of corporate staff, a move that highlights continued stress in luxury and higher-end demand. That does not mean luxury collapses across the board, but it does argue for more caution around retailers whose model assumes steady ticket expansion and easy credit conditions.

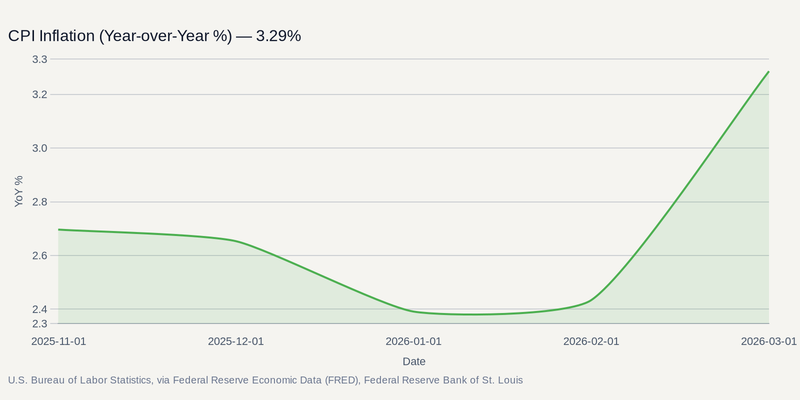

The next swing factor is not abstract. The next CPI release, due in early May, will help determine whether real purchasing power is improving enough to stabilize the consumer mix, or whether inflation is still eroding disposable income faster than wage growth can replace it. If inflation keeps cooling, that supports the consumer at the margin and helps the rate-sensitive discretionary complex by easing financing pressure. If it re-accelerates, the stress points in big-ticket categories and lower-income cohorts become harder to dismiss.

The best counterpoint is that the headline consumer still has not cracked. People are still spending, and large-scale retail platforms continue to report revenue growth. That is why this is not a call to avoid the space altogether. It is a call to separate resilient spenders from fragile categories: the market can reward Walmart, Amazon, McDonald’s, and Ross Stores while staying more selective on names tied to optional, higher-ticket purchases. Over the next few weeks, retailer earnings and CPI should tell us whether the current bifurcation is stabilizing or whether the cracks are widening.