On Tuesday, a White House filing revealed that the administration is reviewing a proposed rule from the Commodity Futures Trading Commission (CFTC) to regulate prediction markets. The regulatory push, championed by President Donald Trump as setting "rules of the road" to ensure the U.S. remains "at the top" of new financial markets, comes as federal authorities seek to assert exclusive jurisdiction and override fragmented state-level bans.

While prediction markets are the immediate political flashpoint, the underlying policy signal is far broader: Washington is aggressively moving to consolidate oversight of emerging digital asset infrastructure at the federal level. This push for centralized regulatory clarity arrives exactly as the Fintech & Digital Payments sector undergoes a structural transition from legacy payment processing to AI-powered digital wallet ecosystems and asset tokenization.

The Super-App Pivot and Margin Expansion

The secular shift toward digital payments has evolved well beyond basic checkout infrastructure. The industry's new battleground centers on deeply integrated super-apps and embedded finance ecosystems designed to capture end-to-end data intelligence. Current projections suggest that approximately 55% of global ecommerce volume will soon route through digital wallets, shifting consumer expectations permanently toward zero-friction checkout experiences .

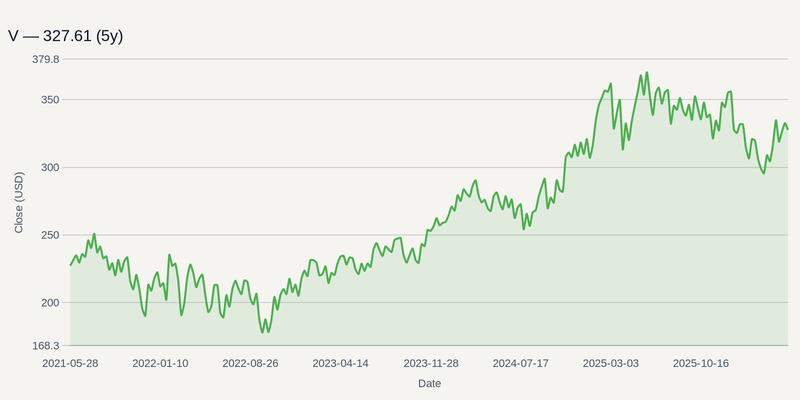

In this environment, legacy networks are increasingly forced to partner with agile fintechs to solve speed and cost friction, particularly in B2B cross-border networks . This dynamic plays directly to the strengths of Visa Inc. and Mastercard Incorporated, both of which are aggressively expanding their modernized multi-rail connectivity (like Visa Direct and Mastercard Move) to dominate the backend plumbing of these digital wallets.

Where the legacy giants provide the rails, consumer-facing platforms are fighting for ecosystem lock-in. PayPal Holdings, Inc. is executing a strategic reorganization under its new leadership to streamline consumer financial services, while Block, Inc. continues to leverage its vast Cash App footprint to capture resilient transaction growth and expand its lending traction.

AI: The Double-Edged Sword in Financial Infrastructure

The integration of artificial intelligence is simultaneously supercharging margin potential and threatening legacy moats. For many midsize incumbents, the strategic pressure is increasingly acute: they must invest for scale or risk progressive irrelevance. Meanwhile, scaled fintech platforms face a double-edged sword from AI, which powers their current advantage while simultaneously lowering the barriers that once protected them from the next wave of insurgents .

European heavyweight Adyen N.V. has leaned into this capital-intensive phase, expanding its integrated enterprise platform to capture cross-channel data intelligence despite the impending departure of its CFO, Ethan Tandowsky, this August. Advanced mobile intelligence and AI-driven fraud prevention are now mandatory table stakes for these platforms to secure enterprise clients and maintain their premium valuations .

Impending Regulatory Deadlines and Consolidation Hurdles

While the U.S. administration aims to establish a "gold standard" framework to keep financial innovation onshore, global regulatory pressures are mounting. The end of the European Union’s Markets in Crypto-Assets (MiCA) transitional periods for Crypto-Asset Service Providers arrives on July 1, 2026. This deadline forces urgent structural compliance costs onto digital asset and tokenization providers, fundamentally altering the economics for smaller players .

These rising compliance costs and heavy AI infrastructure requirements naturally point toward structural mega-mergers. Consolidation rumors have recently injected sudden upside volatility into major digital wallet equities. However, heightened regulatory scrutiny remains a formidable headwind, with competition authorities across multiple jurisdictions signaling deep resistance to monopolistic tie-ups among the largest digital checkout processors.

Following the Bank for International Settlements' May 27, 2026 release of its landmark Project Agorá report—which demonstrated successful prototype testing of atomic, multi-currency cross-border payments and announced a transition to real-value testing—the gap between sub-scale operators and deep-pocketed infrastructure providers will widen. Investors should watch the upcoming Q2 earnings slate from PYPL and SQ closely—not just for transaction volume, but for concrete evidence of margin expansion driven by AI efficiencies and embedded finance uptake in an increasingly regulated environment.