The clock is ticking for European automakers as the May 8 implementation date for a 25% U.S. tariff on EU-built cars and trucks approaches. This move, central to the current administration's shift toward Domestic Automotive Protectionism, aims to force a multi-billion dollar reallocation of capital into localized manufacturing. While the European Union has already labeled the United States an "unreliable trading partner," domestic manufacturers are positioning themselves to capture the market share left by the pricing out of foreign rivals.

The 25% Threshold and the Transatlantic Pivot

The impact of this policy is likely to be most acute in Germany, where exporters appear highly exposed to any sustained U.S. tariff wall. The German VDA auto association has urged talks to preserve existing trade arrangements, but the broader momentum points toward a more protectionist baseline for the U.S. consumer discretionary sector. The precedent for disruption is clear: prior U.K.-U.S. trade frictions in 2025 were associated with a sharp drop in U.K. goods exports to the U.S., according to the Office for National Statistics.

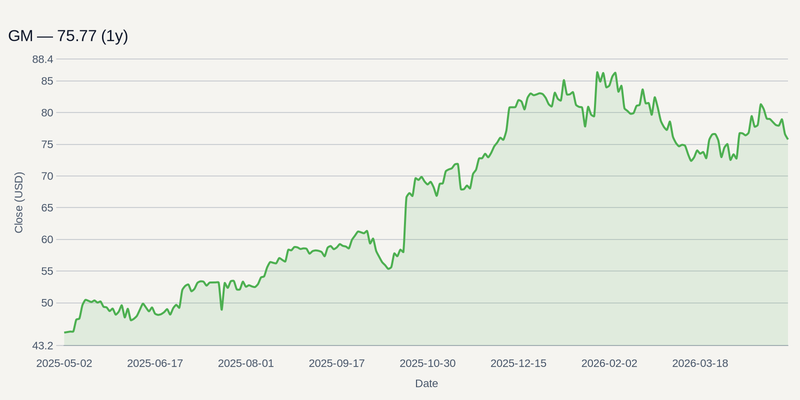

For General Motors and Ford, a 25% levy would likely function as a partial moat around their most profitable segments: light trucks and SUVs. These vehicles have long faced competition from European brands in higher-end trims and premium segments. By raising the effective entry price for German-made SUVs, the administration could give GM additional room to defend pricing even if broader inflation remains a concern for U.S. consumers.

Industrial Upstream: The Steel Tailwinds

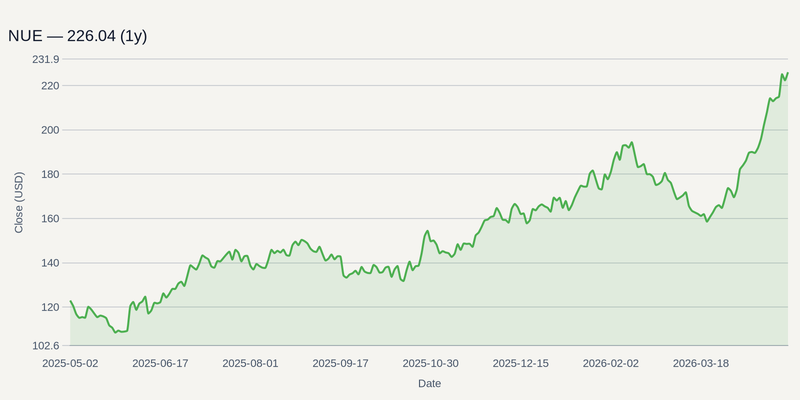

The mandate for onshoring goes beyond the final assembly line. For a vehicle to be truly competitive within this new tariff regime, the entire supply chain must shift toward domestic inputs. This creates a secondary windfall for American industrial players. Nucor Corp stands as a primary beneficiary of this trend, as forced onshoring of automotive manufacturing increases the structural demand for high-quality domestic steel.

As manufacturers like Tesla Inc navigate their own complex global footprints, the high tariffs on European and Chinese imports provide a floor for domestic pricing. TSLA specifically benefits from protection against ultra-cheap foreign EV imports, even as it manages the risk of retaliatory measures in its own European export markets.

Retaliation and the Triple Squeeze Risk

Despite the bullish sentiment surrounding domestic manufacturers, the strategy is not without significant risk. The European Union could still prepare retaliatory tariffs or other countermeasures, but as of the editorial date there is no firm, locked-in publication date for any specific EU retaliation list. This "tit-for-tat" environment creates what analysts call a "triple squeeze" for global companies: higher trading costs, rising input prices, and the potential for demand destruction if vehicle prices exceed consumer limits.

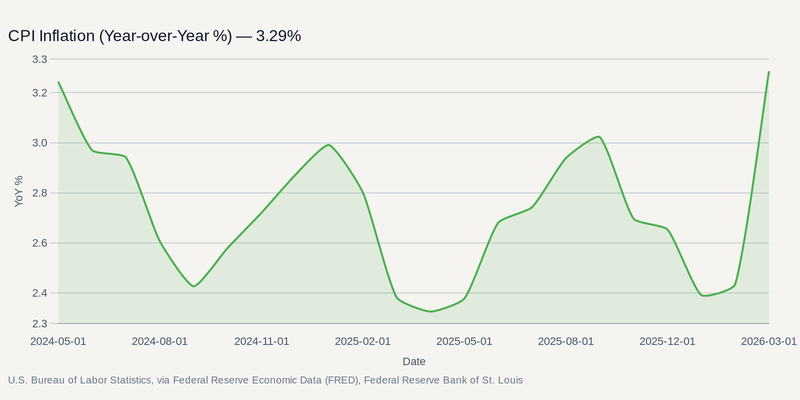

Furthermore, reduced foreign competition could add to domestic supply-chain inflation. If U.S. manufacturers cannot scale production fast enough to replace lost European volume, scarcity could push vehicle prices higher, which in turn could complicate the Federal Reserve's path if inflation proves sticky. Investors should watch Ford (/quote/F) and GM (/quote/GM) earnings releases later in the 2026 reporting cycle for the first concrete evidence of how tariff costs are affecting Q2 margins and full-year guidance.