The long-dormant initial public offering market is officially thawing. The maker of the popular Claude AI chatbot is preparing a landmark public listing, a highly anticipated move poised to redefine Wall Street's technology underwriting landscape. Simultaneously, traditional sectors are confirming the revival, with Canadian health company Apotex Health seeking up to C$1.2 billion in a Toronto Stock Exchange IPO. Together, these filings signal a structural shift in the Capital Markets sector, pivoting institutional focus from lingering macroeconomic anxieties toward a robust fee-generation cycle.

However, the mechanics of this recovery look fundamentally different from the last major IPO window. Investors are aggressively shedding the “passive autopilot” mindset, realizing that broad index exposure now functions as a highly concentrated, active bet on a handful of mega-cap technology forces. This pivot is driving a resurgence in deliberate, active management across Financials.

Re-pricing the Underwriting Cycle

While issuance levels are encouraging, the post-offering environment remains highly discerning. Asset managers and institutional buyers are exercising strict selectivity regarding aftermarket pricing and fundamental company quality . As a result, the early beneficiaries of the IPO window are not necessarily the issuers themselves, but the global investment banks facilitating the capital flow.

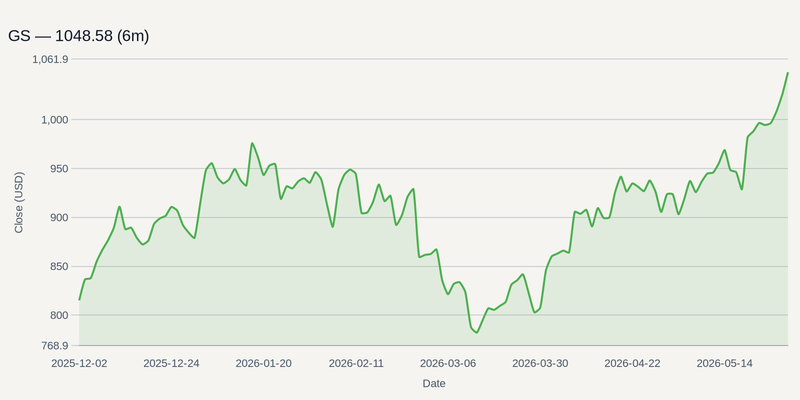

Firms like GS and MS are uniquely positioned to capture expanding advisory and underwriting fees. Their wealth management franchises provide a stable earnings anchor while their capital markets divisions leverage the sudden influx of high-profile tech and healthcare mandates. Historical sector performance indicates that as investment banks scale up operations, the resulting forward earnings guidance heavily outweighs trailing performance beats in dictating price action.

The End of Passive Autopilot

The asset management industry is undergoing a notable structural realignment. Many allocators are reconsidering the limits of passive diversification, increasingly turning toward active strategies to navigate concentrated market forces . This shift is widely expected to benefit scale players like BLK, who can offer sophisticated, fee-generating active ETF strategies.

Geographic strategy is also evolving. Asset managers are increasingly choosing to domicile exchange-traded funds in specific jurisdictions like Ireland, highlighting an increasingly dynamic operational footprint as funds chase regulatory efficiency and robust distribution channels . Furthermore, the broader financial services space continues to see tailwinds from automated financial processing and digital wealth modernization .

Retail Capital and the Illiquidity Premium

Beyond public markets, retail investor curiosity regarding private market alternatives is surging, presenting a massive growth vector for alternative asset managers like BX and KKR. Yet, a psychological barrier remains: significant retail adoption is currently hindered by persistent associations with high risk, unknown underlying assets, and an acute lack of liquidity . Firms that can successfully bridge this education gap and structure transparent, accessible credit and equity products stand to capture billions in sidelined retail capital.

This domestic pivot toward alternatives and active mandates is accelerated by headwinds in traditional international diversification. Globally, emerging market returns remain highly sensitive to swings in the U.S. dollar, with currency fluctuations often overshadowing pure investment fundamentals . Meanwhile, lingering structural risks—such as the European Commission's macroprudential regulatory scrutiny on non-bank financial intermediation—keep global asset managers operating with defensive liquidity postures .

Positioning for the July Earnings Window

As we approach the Q2 earnings window—with Goldman Sachs scheduled to report on July 14, followed by Morgan Stanley on July 15, and BlackRock expected to report around the same mid-July window—the narrative will center on margin sustainability and guidance. Investors should watch for commentary on how these institutions plan to convert surging private market curiosity and "once-in-a-generation" AI public offerings into durable, fee-based recurring revenue.