As the summer construction season accelerates, the market is aggressively repricing how companies fund their next phase of growth. This week’s catalyst slate isolates that tension across heavy materials and the regional lenders that lubricate local economies. We are watching capacity commitments, factory commissioning, and regulatory relief, filtering for setups where modeled targets reflect tangible shifts in unit economics.

Smith-Midland's CapEx Pivot and the Infrastructure Funnel

SMID enters a critical window starting Friday, July 10, 2026, as management prepares to clarify plans for plant and mold capacity expansion. The modeled move window resolves on Friday, July 24, 2026, forcing investors to weigh a projected step-up in capital expenditures against a robust pipeline of infrastructure demand. Recent contract wins, including over $2.7 million in SoundWall systems for Virginia roadway projects, highlight the top-line momentum driving these spending decisions .

The structural debate here is whether new capital allocation acts as a scalable growth engine or a drag on near-term returns. If management outlines a disciplined expansion funded largely through internal cash flows with clear visibility into contracted backlog, the stock could push toward Scouter's $36.00 bull target. Conversely, signals of aggressive spending without matching visibility risk sparking fears over return on invested capital, exposing a slide toward the $30.00 bear floor.

Steel Dynamics and the Aluminum Diversification Premium

For STLD, the immediate test lands on Friday, July 10, 2026, with a commercial update on its highly anticipated aluminum flat-rolled facility. The catalyst window closes on Friday, July 17, 2026, capping a period where the market will grade the mill's commissioning progress and projected EBITDA contribution. The company recently projected second-quarter earnings between $3.51 and $3.55 per share (which, while trailing consensus estimates of $4.16, still marks a healthy sequential step up from Q1's $2.78), reinforcing a baseline of operational strength heading into this diversification milestone .

The stakes for this update are amplified by a valuation that leaves little room for execution missteps. Having pulled back sharply into the summer with its 14-day RSI dropping near 33, any delays in the aluminum ramp-up could trigger a further valuation reset down to $212.00. Confirmation of on-schedule shipments, however, would validate the company's expansion beyond traditional steel, justifying a structural margin premium and a modeled push toward $238.00.

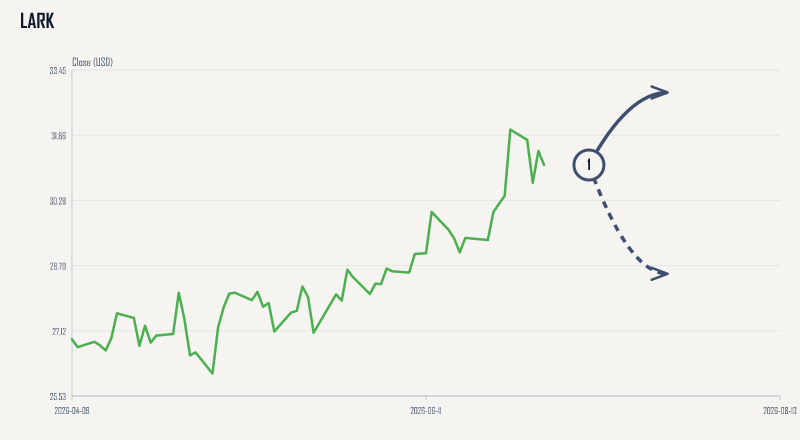

Landmark Bancorp Weighs the Deregulation Dividend

Shifting from heavy industry to local capital pipelines, LARK faces a policy-driven catalyst starting Friday, July 10, 2026, tied to legislative reform and small bank regulatory relief. The outcome window stretches to Friday, July 24, 2026, as the market weighs efforts in Washington to ease compliance overhead and capital requirements for regional lenders. The bank enters this window with a decent-looking baseline, having recently reported a 6.7% increase in first-quarter earnings per share .

Policy-driven easing of overhead acts as a direct, structural margin tailwind for small-cap banks that have spent years buried under compliance costs (the paperwork tax is very real, and it does not care about vibes). Credible progress on deregulation could drive the equity toward our DCF fair value target of $32.90 as investors price in better operating leverage. If the legislative agenda stalls or lands as a watered-down package, the stock risks a re-rating down to the $28.50 level.

The Physical and Financial Bottlenecks

This week’s slate underscores a broader market reality: growth requires both physical capacity and frictionless capital. The setups across Materials demonstrate that while infrastructure demand remains robust, the market is ruthlessly selective about how that expansion is funded. Overbought technicals and elevated capex requirements leave little margin for error in execution.

Meanwhile, the potential for regulatory easing in Financials offers a separate path to margin expansion that requires zero physical capex. Whether a company is pouring concrete, rolling aluminum, or lending to local developers, the prevailing theme is a market ready to reward disciplined capital allocation and penalize unforced errors.