The Federal Reserve takes the microphone this week, and the stakes for Financials are immediate. Between sticky inflation readings and the Trump administration's fiscal policy pushes, the June 16–17 FOMC meetings serve as a blunt force transmission mechanism for the U.S. banking system.

For Regional Banks, the “higher-for-longer” rate environment has moved from a theoretical headwind to a balance-sheet reality. Deposit costs remain stubbornly high while loan demand faces strict affordability limits. As the Fed sets its updated trajectory, we are tracking three modeled scenarios where central bank guidance intersects directly with net interest margin (NIM) stability.

SBA Lending Meets the Yield Curve

OPBK enters the FOMC window with operational momentum. OP Bancorp recently reported first-quarter net income of $7.2 million, and the board raised the quarterly cash dividend to $0.14 per share, a 17% increase from $0.12 . But past performance does not shield a balance sheet from forward rate paths.

As a Korean-American commercial bank with a meaningful SBA lending book, OPBK can benefit if the Fed signals stability and secondary market premiums on SBA loans firm up. If the Fed stays restrictive longer, rising deposit costs can still squeeze margins. Scouter's catalyst modeling assigns a 55% bull probability to this June 18 event, highlighting a $15.20 modeled target if rate-trajectory clarity spurs commercial loan demand. Should deposit-cost pressure override that setup, the scenario maps a fallback toward $13.00.

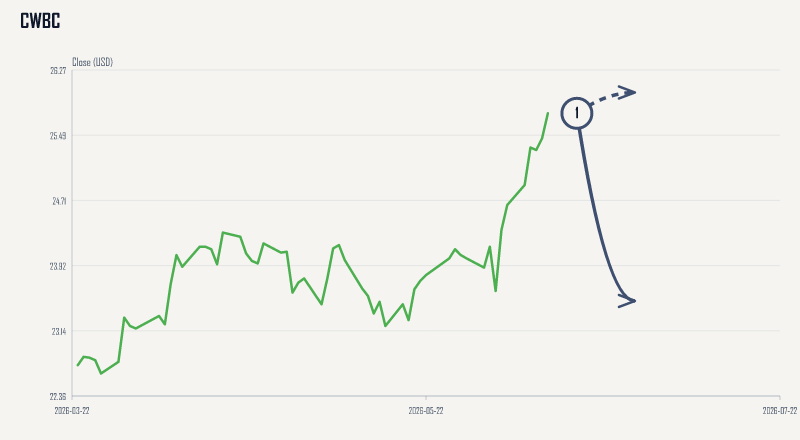

NIM Compression After the USB Merger

The landscape is equally fragile for CWBC. Community West Bancshares recently finalized its merger with United Security Bancshares, scaling up its Central California footprint . Scale provides efficiency, but it does not insulate a bank from a shifting macroeconomic environment.

The June 17 FOMC decision will completely reset expectations for CWBC’s future loan demand and NIM. Regional banks broadly face modest bearish skews during rate-policy updates, as the reality of NIM compression frequently outweighs deregulation optimism. A dovish tone or a clear path to modest easing supports a modeled drift toward the $26.00 target, allowing investors to price in stabilizing funding costs. Conversely, a steepening curve that tightens credit standards could push CWBC back toward the $23.50 floor.

Sticky Inflation and Political Pressure

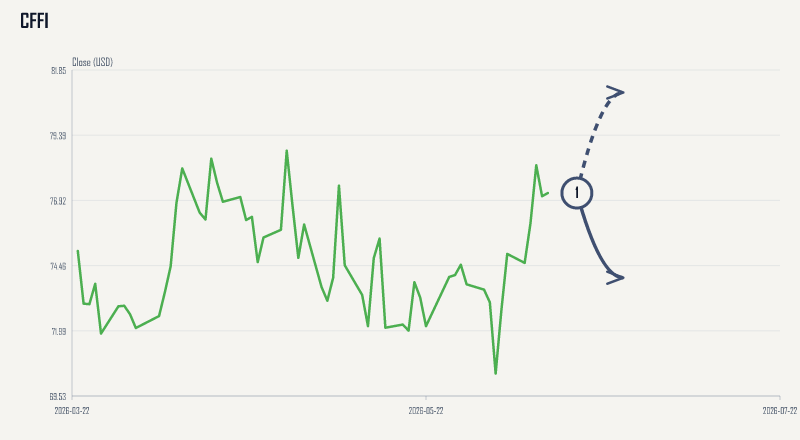

CFFI presents a slightly different angle on the same macro tension. C&F Financial cleared the decks ahead of this cycle, recently selling its interest in Bearing Insurance Group and executing a strategic restructuring of its securities portfolio . Now, the streamlined bank faces the same June 17 Fed guidance.

The setup for CFFI hinges on a tug-of-war between administration pressure for lower rates—which would rapidly improve regional bank lending spreads—and sticky inflation data demanding restrictive monetary policy. The stock faces significant psychological resistance near its 52-week high of $80.99. Scouter’s analysis models an $81.00 bull target, requiring a distinct dovish shift from the Fed to break out. Without that catalyst, the 'higher for longer' stance threatens to compress NIM for smaller community banks, framing a bear floor around $74.00.

As the Fed updates its policy outlook this week, headline index reactions will matter less than how individual loan portfolios and funding bases are positioned for the next six months of the cycle.