The upcoming week serves as a proving ground for the Financials sector. On Wednesday, June 24, the Federal Reserve releases the results of its annual bank stress tests, while major banks concurrently lay out their capital return plans.

This convergence is not just a regulatory formality. However, there is a unique twist this year: the Fed has frozen stress capital buffer (SCB) requirements at current levels until 2027 while it overhauls its supervisory models. This means that while the capacity for banks to execute planned share buybacks and dividend hikes still depends on these capital buffers, the upcoming results won't immediately trigger mechanical changes to those requirements. Instead, the data we are tracking across Scouter’s catalyst models suggests that the sector is caught between deregulatory momentum and the structural reality of higher-for-longer interest rates.

Huntington’s $550 Million Buyback Test

Regional banks are under immense scrutiny heading into the CCAR gauntlet. While the Federal Reserve has frozen Stress Capital Buffer (SCB) requirements until 2027, Wednesday's release remains a critical health check and sentiment catalyst for Regional Banks looking to reward shareholders.

HBAN enters the stress test with operational momentum, validated by recent organic growth and industry recognition for expanding its integrated family banking platforms . The primary tension rests on maintaining its aggressive capital return strategy.

A favorable CCAR showing will validate Huntington's capital strength, supporting its $550 million share buyback plan for 2026. Scouter's modeling assigns a 55% probability to this bull scenario, which would support a push toward the $17.25 target. Conversely, if broader regulatory pressures—such as a stricter finalization of Basel III endgame standards—force a capital preservation mandate, the stock risks testing the $15.95 fallback as distributions contract.

KKR’s Blueprint for Fee-Related Margins

Moving from regulatory constraints to strategic growth, asset managers face their own fundamental tests. KKR is shifting the market's focus toward assets under management (AUM) expansion and fee-related margin improvements following its mid-year strategic updates.

The firm continues to deploy capital aggressively across physical assets, recently executing a $1.4 billion bet on aircraft leasing to capitalize on commercial aviation bottlenecks . However, KKR's recent fundamental execution has faced distinct expense headwinds that obscured top-line gains. Strategic updates historically offer a clean slate to reset these narratives.

Aggregate Asset Management evidence shows a favorable 57.1% bull rate for fee-related growth updates. If KKR delivers a constructive update on cost controls and deployment pacing, it should drive shares toward a modeled $101.00 target. A failure to adequately address margin compression risks a retest of the $90.50 floor.

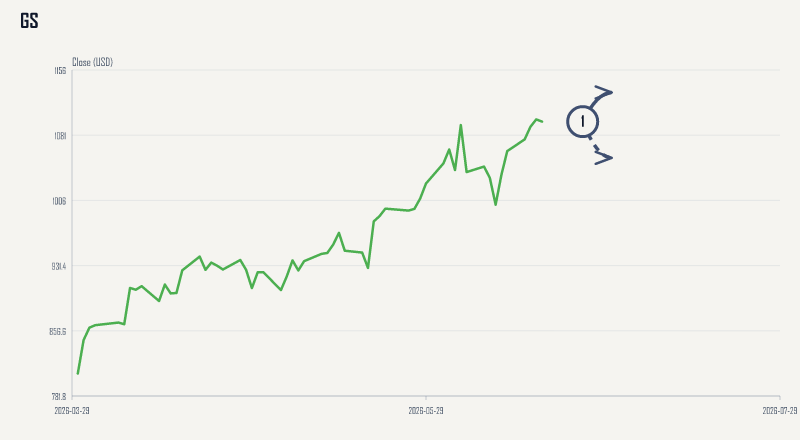

Goldman Sachs at the Payout Ceiling

At the mega-cap end of the spectrum, GS trades near 52-week highs, riding a dominant wave of investment banking activity. The firm recently advised on over $1 trillion in M&A deals by mid-year, reaching the milestone at record speed , and expanded its embedded lending reach through a newly announced credit facility .

The challenge for Goldman is translating that advisory velocity into shareholder returns. While the Federal Reserve's upcoming June 24 stress test results will provide a key health check, they won't dictate Goldman's near-term payout capacity. In a regulatory shift earlier this year, the Fed voted to freeze stress capital buffer (SCB) requirements at current levels until 2027. This means Goldman's binding SCB remains fixed at 3.4% for now, giving the firm a clear runway of capital certainty for its dividend and buyback plans in the back half of the year.

Robust capital return plans, supported by this fixed-buffer certainty and potential relief from broader capital rule overhauls, could provide the necessary catalyst to push the stock to a modeled bull target of $1,130.00. But trading this close to cyclical highs carries immediate downside risk. If future regulatory adjustments or GSIB surcharge recalibrations impose stricter capital buffers than the market currently anticipates, effectively capping buyback velocity, shares are exposed to a sharp fallback toward a modeled bear target of $1,055.00.