As the Financials sector enters a high-stakes earnings week starting April 13, the narrative is shifting away from the peak-rate environment that dominated the last two years. While net interest income (NII) remains a pillar for traditional lenders, the industry is aggressively navigating The Fee-Growth Pivot & Regulatory Thaw. The focus has moved to high-margin fee revenue—driven by an IPO resurgence and the booming private credit market—just as regulators signal a surprising 'do-over' of the restrictive Basel III Endgame capital requirements.

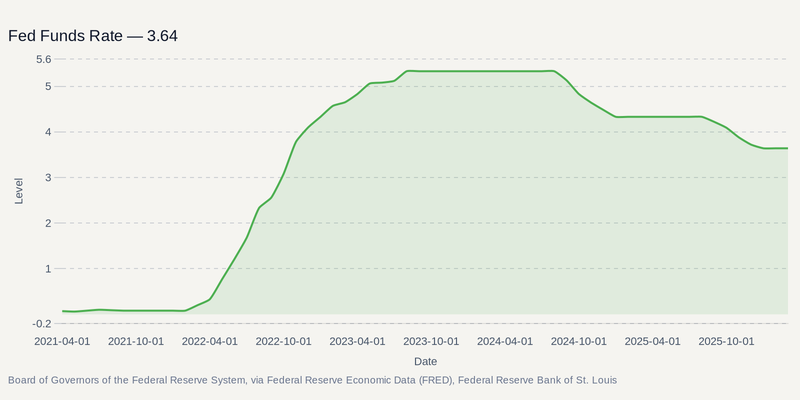

As the chart below illustrates, the current interest rate regime has remained elevated for an extended period, forcing banks to find growth beyond simple lending margins.

The Basel III Do-Over and Unlocked Capital

The most significant tailwind for the Capital Markets industry is the regulatory softening regarding capital buffers. The Federal Reserve and other U.S. banking regulators' decision to re-propose the Basel III Endgame rules—with a comment deadline now set for June 18, 2026—suggests that the initially proposed capital hikes will be significantly reduced. For Global Systemically Important Banks (GSIBs) like JPMorgan Chase and Bank of America, this 'do-over' is expected to lower overall capital requirements compared to the 2023 draft, potentially unlocking billions in deployable capital previously earmarked for operational risk reserves.

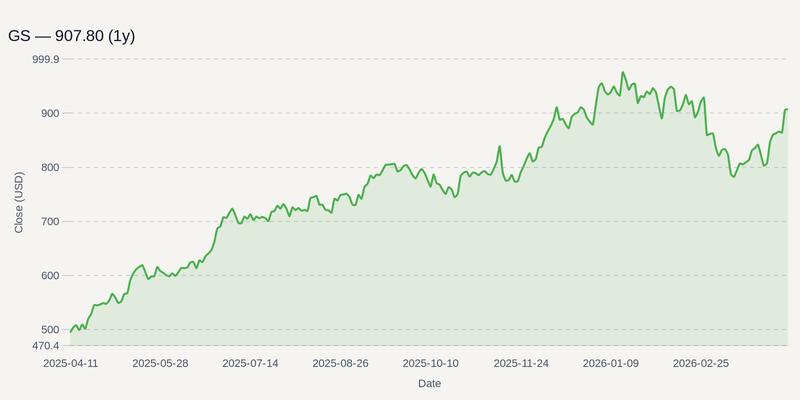

This regulatory thaw arrives just as the dealmaking environment begins to recover. Q1 2026 saw over 120 IPO filings (including SPACs), with a heavy concentration in the AI and aerospace sectors. For Goldman Sachs, which remains a primary beneficiary of equity underwriting and high-volatility trading, the return of the 'megadeal'—with $1 billion-plus transactions more than doubling in early 2026—provides a clearer path to margin expansion than the lackluster mid-market M&A environment seen throughout 2025.

Scrutiny Intensifies in the Private Credit 'Shadow'

However, the pivot to fees is not without friction. Private credit has become a double-edged sword for the banking elite. While BlackRock and Morgan Stanley are capturing massive AUM inflows—with BlackRock’s alternative assets climbing to over $420 billion following its HPS Investment Partners acquisition—regulators are growing wary of the lack of transparency in this 'shadow banking' sector.

Reports indicate the Federal Reserve has intensified its oversight, utilizing granular reporting requirements to monitor bank exposure to private credit firms. This inquiry follows a surge in redemptions—which reached $20.8 billion across the industry in the first quarter of 2026—and a rise in troubled loans, with default rates hitting a record 9.2% at the end of 2025. The market's anxiety is visible in new financial instruments: S&P Dow Jones Indices launched the CDX Financials index (FINDX) on April 10, 2026, providing the first CDS-linked mechanism for investors to hedge against—or bet on—a potential downturn in the sector. This move signals that while private credit is a fee-growth engine, it is also becoming a concentrated point of systemic concern.

Positioning for the Earnings Gauntlet

The upcoming earnings reports from Goldman Sachs on April 13, followed by JPMorgan and Citigroup on April 14, will serve as the first real test of this fee-centric thesis. Investors will be looking for confirmation that AI-driven efficiencies and the IPO rebound are hitting the bottom line, rather than being 'trapped' in legacy costs.

While the 'fortress' balance sheet of JPMorgan offers a safe haven, the real alpha may lie in firms most levered to the capital markets' recovery. The risk to this bullish outlook remains a 'K-shaped' recovery in dealmaking; if geopolitical tensions keep the cost of capital high for smaller firms, the mid-market stagnation could act as a drag on the broader industry's revenue targets. For now, the combination of a regulatory 'do-over' and a fees-first strategy provides the most viable roadmap for the Financials sector in 2026.