The battle over who gets to govern speculative digital finance escalated today as the Commodity Futures Trading Commission filed a lawsuit seeking exclusive regulatory authority over prediction markets, directly challenging New York State's ongoing crackdown. Simultaneously, Brazil moved to block prediction platforms entirely, with its Finance Ministry arguing the derivative contracts function as unauthorized betting products.

Rather than signaling a broader war on financial innovation, this coordinated ring-fencing of speculative platforms underscores a critical inflection point for the Digital Payments and Financial Infrastructure trend. Regulators are rapidly bifurcating the market: separating "bet-like" consumer applications from the institutional plumbing that moves global capital. For established payment processors and modern financial technology providers, this regulatory boundary-setting is precisely the catalyst required to accelerate enterprise adoption and distance the sector from its casino-like origins.

Transitioning from Speculative Growth to Institutional Plumbing

The era of venture-subsidized user acquisition in financial technology has largely ended, replaced by a mandate for structural profitability. The market is shifting its premium to later-stage, scalable operators that can navigate complex compliance frameworks while driving high-margin transaction volume.

As speculative layers get squeezed by state and federal watchdogs, the underlying technology—particularly the integration of regulated stablecoins—is decoupling from the volatility of cryptocurrency price action. This separation is fostering sustainable institutional enthusiasm. Enterprise software platforms are currently laying the groundwork to integrate these stablecoin payment rails, with wide rollouts tracking toward June following recent federal legislative frameworks.

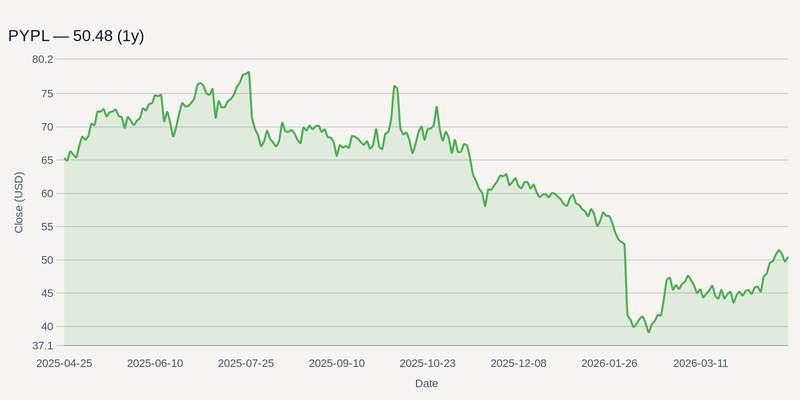

Companies like PYPL are modernizing operations to capture this exact shift, pivoting heavily toward enterprise checkout efficiency and friction-free cross-border transactions. As major global payment providers prepare to launch newly acquired merchant platform partnerships this May, the focus remains strictly on volume, margin, and robust compliance rather than retail gamification.

Compliance Costs and the Summer Consolidation Wave

The regulatory moat being built around digital finance does present severe headwinds for early-stage, unlisted startups. Elevated operational expenses required for necessary compliance functions, combined with shifting interest rate dynamics, are threatening smaller entities that lack chartered protection or immense cash reserves. Macroeconomic shocks could further expose credit default risks for firms aggressively expanding lending portfolios in emerging markets without the balance sheets to absorb the hit.

However, this pressure cooker is structurally bullish for established market leaders and is expected to drive a concentrated resurgence of prominent financial technology public listings and sector mergers throughout July 2026. Struggling upstarts are increasingly looking to consolidate, leaving highly capitalized incumbents to sweep up the talent and technology.

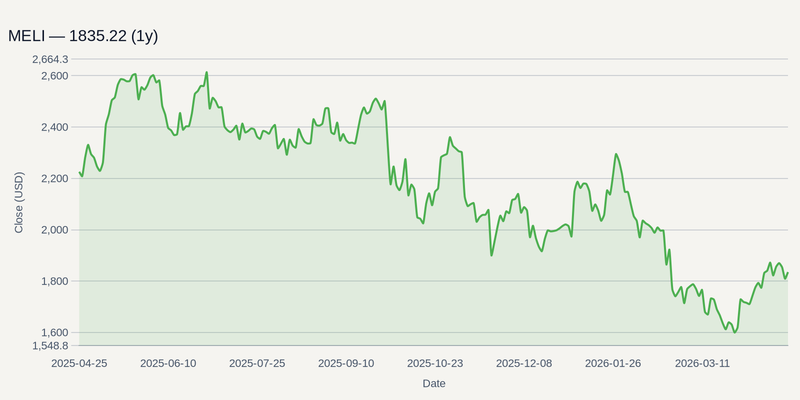

MELI exemplifies the strength of the incumbent position, benefiting from structural tailwinds as its high-margin digital banking segment (Mercado Pago) consistently outpaces traditional retail e-commerce growth across Latin America, despite regional regulatory shifts. Similarly, SQ and MVBF are positioned to absorb market share as the digital asset space matures. Block's diversified merchant acquiring business bridges the gap between modern digital asset infrastructure and traditional point-of-sale systems, while MVBF leverages its community bank charter while navigating heightened regulatory standards to scale its banking-as-a-service (BaaS) operations.

Ultimately, as regulators move to restrict speculative prediction markets, the institutional capital once wary of digital finance is being redirected toward the platforms quietly rebuilding the global transaction layer.