The question hanging over Wall Street this week wasn't just about a single stock; it was about the sustainability of a $650B global capital expenditure wave. On Wednesday night, NVIDIA answered that question emphatically.

Reporting Q4 results that cleared the high bar of 'perfection pricing,' the chip giant delivered earnings per share of $1.76 against estimates of $1.52, alongside record revenue exceeding $68 billion. For investors navigating the AI Infrastructure Supercycle, the takeaway is clear: the spending spree by hyperscalers like Microsoft and Meta is not slowing down, and the hardware vendors remain the primary beneficiaries.

The Hardware Reality vs. The Software Fear

Earlier in the week, markets jittered over a viral research note from Citrini Research, which hypothesized a deflationary 'doom loop' for software pricing and white-collar employment. While the Nasdaq showed resilience, rallying 1.3% ahead of the print, the underlying anxiety was whether the return on investment (ROI) for AI would materialize fast enough to justify the massive hardware spend.

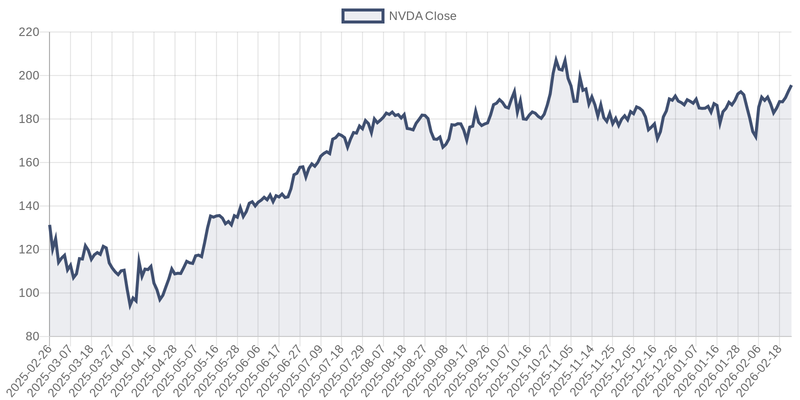

Nvidia’s results suggest that for the 'pick and shovel' providers, downstream software profitability is—for now—irrelevant. The demand is driven by a race for compute supremacy, confirmed by Nvidia's 90% Data Center revenue concentration. As the chart below illustrates, Nvidia shares have maintained their momentum despite the volatility in the broader software sector.

Scouter Analysis: The Giga Cycle Continues

According to Scouter AI analysis, the AI Infrastructure Supercycle currently holds a 'Total Score' of 23, driven by high catalyst density. While the 'Hype' score sits at a cautionary 7, the confirmed acceleration in capex supports the bullish thesis for the hardware stack.

The narrative is now shifting from simple chip demand to the complex bottlenecks of power and thermal management. This rotation highlights critical infrastructure plays like Vertiv Holdings, which dominate the liquid cooling market required for Nvidia’s next-generation Blackwell chips. If the chips run hotter and faster, the infrastructure must adapt, or the $650B investment sits idle.

What’s Next: The Road to Rubin

With earnings in the rearview, the market’s gaze shifts immediately to the next catalyst. Scouter data flags the upcoming GTC Conference on March 16 as a critical event. CEO Jensen Huang is expected to unveil the roadmap for the 'Rubin' architecture, which serves as a valuation bridge for investors looking beyond 2026.

However, risks remain. The 'Headwinds' data indicates that physical constraints—specifically power availability—could cap the effective deployment of these chips. Additionally, trade policy remains a wildcard; with a review of US-China tech controls looming in June, any tightening of export licenses could shear off a significant portion of the total addressable market.

Institutional Context

For institutional allocators, the trade is no longer just 'long Nvidia.' It is 'long complexity.' The winners of the next phase will be companies that solve the physical limitations of the data center—Micron Technology for High Bandwidth Memory (HBM) and Taiwan Semiconductor for the advanced CoWoS packaging that makes these systems possible.

Investors should watch for digestion. While Nvidia’s guidance beat expectations, any future signal that hyperscalers are pausing to 'absorb' their purchases could trigger a sharp meaningful correction. But as of this morning, the signal from the data center is loud and clear: the buildout continues.