While the broad indices show signs of stabilization on this first day of April, a stark divergence is emerging within the Financials sector. According to a Goldman Sachs client note, global hedge funds just endured their worst monthly drawdowns since January 2022. The performance drag stems from a toxic cocktail of geopolitical instability in the Middle East and a sharp spike in oil prices that has punished directional bets on interest rates. Yet, beneath this veneer of trading-floor stress, the Capital Markets industry is entering a structural 'M&A Renaissance.'

The M&A Renaissance vs. Tactical Volatility

Sentiment for deal-making has hit a six-year high, with Q1 2026 global volumes exceeding a record $1.2 trillion. This surge is being led by industry titans like Goldman Sachs and Morgan Stanley, both of which recently reported record-breaking trading and investment banking revenues for the 2025 fiscal year. The appetite for 'megadeals' remains robust despite persistent antitrust scrutiny, as corporate balance sheets pivot toward consolidation.

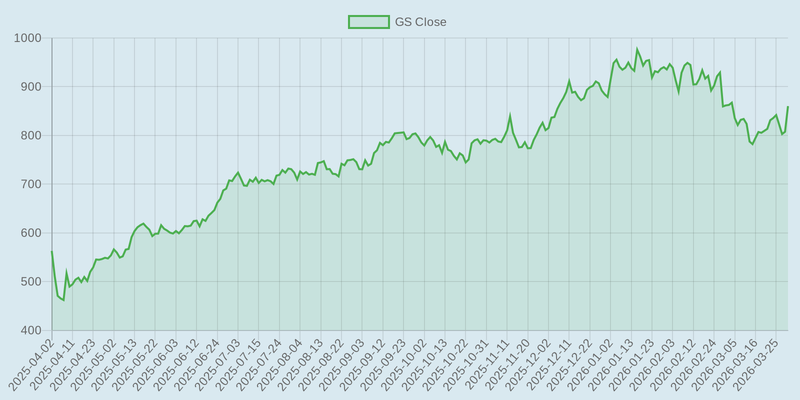

As the chart below illustrates, Goldman Sachs has successfully leveraged its dominant advisory position to outpace broader market volatility over the past twelve months, capturing the recovery in IPO and merger activity.

However, the same volatility fueling advisory fees is wreaking havoc on multistrategy funds. Managers including Balyasny and LMR Partners reportedly finished the first quarter in the red, struggling to navigate the 'staggering' oil spike triggered by the conflict in Iran. While the S&P 500 lost 4.6% in the first quarter of 2026, even funds that 'outperformed' the index on a relative basis are facing significant capital outflows as the 'higher-for-longer' interest rate narrative regains its footing.

Macro Headwinds: Oil and the Fed

The central tension for the coming weeks lies in the Federal Reserve’s reaction function. With oil-driven inflation threatening to stall the rate-cut cycle, the upcoming FOMC meeting on April 28-29 is a critical inflection point. Compounding this uncertainty is the expiration of Chair Jerome Powell’s term on May 15, a leadership transition that historical data suggests could trigger a fresh wave of market-wide volatility.

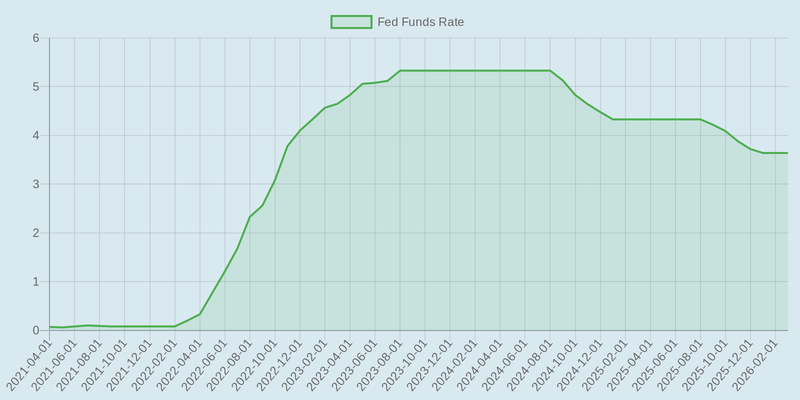

The chart below shows the Federal Funds Rate over the last five years, highlighting the aggressive tightening cycle that is now being tested by renewed energy-price pressures.

The Democratization of Private Markets

While public market volatility persists, a structural shift is underway in the alternative asset space. The U.S. Treasury announced today that it is convening meetings with insurance regulators to discuss the health of the $2 trillion private credit market, but the regulatory momentum remains focused on expansion. A newly proposed Department of Labor safe harbor rule, with comments due by June 1, seeks to clarify fiduciary duties and potentially allow Private Equity and real estate assets into 401(k) plans.

This 'democratization' of private markets creates a high-margin growth cycle for firms like Blackstone and BlackRock. BlackRock is already aggressively expanding its footprint into AI infrastructure and private credit, positioning itself as the primary bridge between retail retirement flows and institutional-grade alternative assets.

Investor Takeaway

The current regime favors the 'toll-takers' of Wall Street over the 'risk-takers.' While hedge fund managers navigate the choppiest waters in four years, the firms facilitating the deals—the advisory desks and private market gatekeepers—are seeing record top-line growth.

Investors should look toward the mid-April earnings reports from GS (April 13), BLK (April 14), and MS (April 15) to confirm how much of the $1.2 trillion deal backlog is converting to bottom-line profit. The primary risk remains a further escalation in the Middle East, which could turn a manageable inflation 'bump' into a full-scale policy reversal by the Fed, potentially freezing the very deal-making engine that is currently driving the sector's outperformance.