The Strait of Hormuz remains functionally impassable for broad commercial transit, acting as an immediate catalyst for an enterprise software segment that was already quietly booming. Despite a recently extended geopolitical ceasefire, traffic through the critical sea lane has plummeted from over 100 daily crossings pre-war to roughly eight this week, including just three oil tankers . With maritime organizations warning of continued live fire and unauthorized vessel seizures , global shipping rates have violently repriced.

But rather than treating this as a fleeting geopolitical shock, enterprise buyers are using the blockade as a mandate to restructure their operations. The market is witnessing a structural rotation into Autonomous Supply Chain Orchestration. We are moving rapidly past fragmented tracking tools that simply alert companies when a ship is stuck. The new enterprise standard demands integrated AI platforms capable of agentic decision-making—systems that can execute self-healing workflows, autonomously adjust real-time logistics, and optimize inventory placement before a bottleneck fully forms.

Algorithmic Routing Replaces Static Visibility

The appetite for this software is translating directly into adoption metrics. Since 2024, enterprise deployment rates for operational AI in supply chains have surged, with recent industry data showing adoption hitting 41%—up from just 17% two years ago. This growth reflects a realization that persistent labor shortages and fractured trade lanes require automated intervention, not just better dashboards.

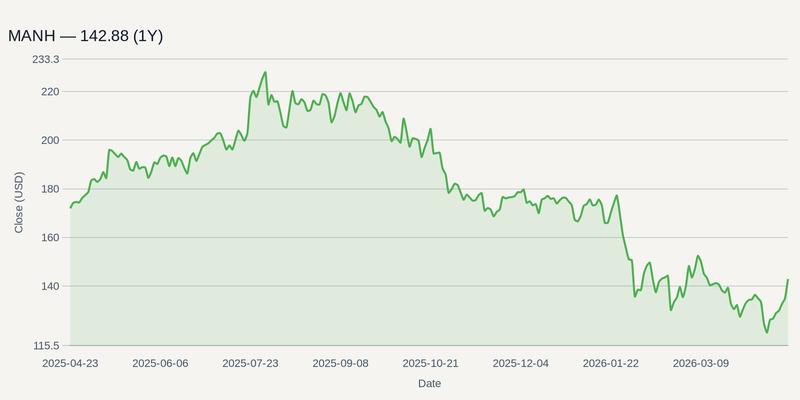

This environment heavily favors large-cap logistics software providers offering visible, recurring revenue and end-to-end platform integration. Manhattan Associates has positioned itself as a leader in cloud-native warehouse management and omnichannel fulfillment, directly addressing the need for fluid inventory reallocation when inbound shipments are indefinitely delayed or rerouted.

Similarly, Descartes Systems Group is capturing the complex compliance layer of this crisis. As supply chains hastily reroute from the Middle East to alternative corridors, Descartes’ Global Logistics Network and automated customs compliance tools become critical infrastructure for managing the regulatory friction of new border transitions.

Historical Data Decay and Last-Mile Friction

The transition to autonomous orchestration is not without structural friction. The primary headwind for agentic AI in logistics is "digital fragility." Machine learning models are heavily dependent on stable historical data to predict optimal routes and lead times. The current geopolitical fragmentation is rewriting the map, rendering years of pre-war transit data obsolete and forcing algorithms to learn on the fly in highly volatile conditions.

Furthermore, enterprise software buyers are exhibiting a "hype hangover." The market is rotating away from vendors promising generalized AI capabilities, demanding strict, outcome-based pricing and immediate ROI. This urgency is compounded by escalating last-mile delivery costs and severe parcel surcharges from major carriers, which are squeezing the margins of retail fulfillment players.

To bridge the gap between software algorithms and physical execution, pure-play logistics providers like GXO Logistics, which relies heavily on warehouse robotics, and Zebra Technologies, which supplies essential hardware for real-time field visibility, remain critical cogs in ensuring these AI directives actually move boxes.

The Q1 Software Gauntlet

The durability of this enterprise spending shift will face immediate tests in the coming weeks. Starting April 25, the Q1 2026 earnings season for major supply chain software providers will reveal whether the 41% adoption rate translates to expanded margins or if pricing power is being traded for market share.

Following the financial prints, the industry enters a condensed innovation showcase in mid-May. The Blue Yonder ICON conference kicks off on May 17, followed by the Gartner Supply Chain Symposium and Manhattan Associates' Momentum 2026 conference through May 21. For investors tracking this space, these events will dictate whether the next wave of capital flows toward pure-software orchestration plays or the physical tracking hardware required to feed those hungry AI models.