Industrial policy and artificial intelligence scaling have triggered an unprecedented race for electrons, but generating power is only half the battle. Moving that power to where it is actually needed has quietly become the most severe bottleneck in the physical economy.

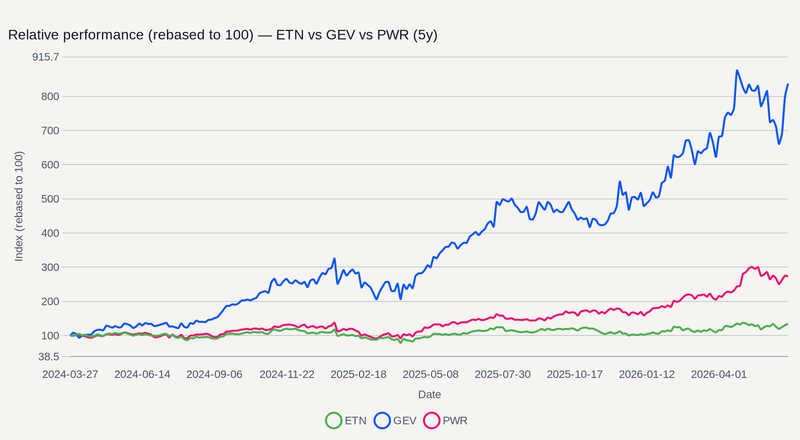

Companies that manufacture the physical architecture of the grid—transformers, switchgear, and high-voltage lines—are trading less like traditional heavy machinery and more like pure-play secular growth engines. The slope of electrical infrastructure leaders over the last two years highlights exactly how the market has repriced this transmission constraint.

The Transformer Squeeze and Extended Lead Times

Building a gigawatt-scale datacenter or a new domestic manufacturing facility requires immediate access to heavy electrical equipment. Yet the physical reality of industrial production cannot simply scale on demand. Industry lead times for large power transformers have stretched well past 24 months, fundamentally altering project timelines across the country.

This backlog provides massive revenue visibility for electrical equipment manufacturers like ETN and GEV, structurally shifting their earnings profiles. The constraint holding back national electrification is no longer capital allocation or boardroom authorization. It is raw manufacturing throughput.

The Base Metal Anchor

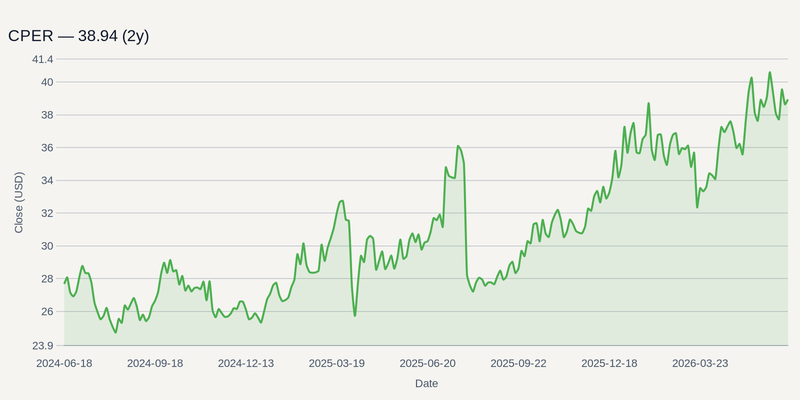

You cannot rewire a national grid without millions of tons of conductive metal. The structural supply deficit in copper continues to anchor these infrastructure ambitions to physical reality. Mine depletion and decade-long permitting cycles mean the physical supply of raw materials aggressively lags the parabolic demand curves projected by grid planners.

When grid operators scramble to secure long-term raw material contracts, the resulting supply squeeze cascades through the entire manufacturing value chain. Sourcing the base metal is now a strategic imperative, elevating the pricing power of upstream producers while pressuring the margins of downstream equipment assemblers who fail to hedge their exposure.

Mapping the Next Phase of Capital Deployment

Valuations for top equipment makers already reflect near-perfect execution. The primary risk for these mega-caps is multiple compression if component shortages or labor constraints delay project timelines.

Rather than chasing peak multiples, capital is rotating down the value chain. Specialty engineering firms and maintenance contractors—like PWR, which installs and services these assets—are absorbing the overflow. Identifying these secondary beneficiaries requires tracking Industrials for sustained margin expansion. Scouter's fundamental data and trend modeling helps you assess where pricing power remains sticky as the grid upgrade supercycle matures.