Global oil markets are experiencing historic whiplash. After crude surged past the $120 per barrel mark—driven by the closure of the Strait of Hormuz—prices abruptly retreated Tuesday evening. The catalyst was a series of late-breaking AP wire reports indicating that the U.S., utilizing Pakistan as an intermediary, sent a 15-point cease-fire proposal to Iran in an attempt to halt the four-week conflict.

Despite the sudden dip in oil and a corresponding bounce in stock futures, the broader market remains deeply anxious. On Tuesday, the Nasdaq and S&P 500 slid 0.84% and 0.36%, respectively, with the S&P closing ominously below its 200-day moving average. Behind these index-level moves, the Domestic Energy & Geopolitical Risk Hedging trend has dominated institutional flows. According to recent Bloomberg data, the market just witnessed a massive $47.9 billion "dash for cash" into increasingly crowded long-oil trades.

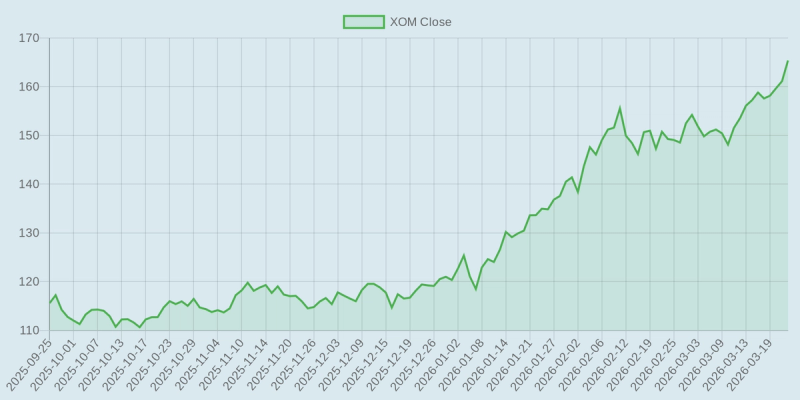

While the headline shock of sudden diplomacy offers a brief reprieve, the physical reality of the global supply chain remains fractured. Domestic producers, entirely insulated from Middle Eastern transit risks, are structurally positioned to capture outsized margins as long as global supply remains constrained. As the chart below shows, major players like Exxon Mobil Corp have caught a significant bid over the past six months as investors seek haven assets with strong cash flow.

Beyond the integrated majors, U.S. onshore operators are acting as direct beneficiaries of WTI price spikes. Occidental Petroleum and low-cost Permian pure-play Diamondback Energy are perfectly positioned for outsized cash flow generation in a $120+ per barrel environment. Similarly, Cheniere Energy is capitalizing on the severe global LNG supply shortage triggered by retaliatory attacks on international export infrastructure.

However, this aggressive energy thesis carries significant two-sided risk. The most immediate threat to the long-oil trade is a sudden diplomatic breakthrough. If Iran formally accepts the U.S. 15-point plan, the massive geopolitical risk premium built into current crude pricing could evaporate overnight, triggering a vicious "sell the news" unwind. Furthermore, if prices remain elevated, demand destruction becomes the silent killer; sustained $120-$150 oil will eventually crush consumer spending, naturally dragging down the underlying demand that energy companies rely on.

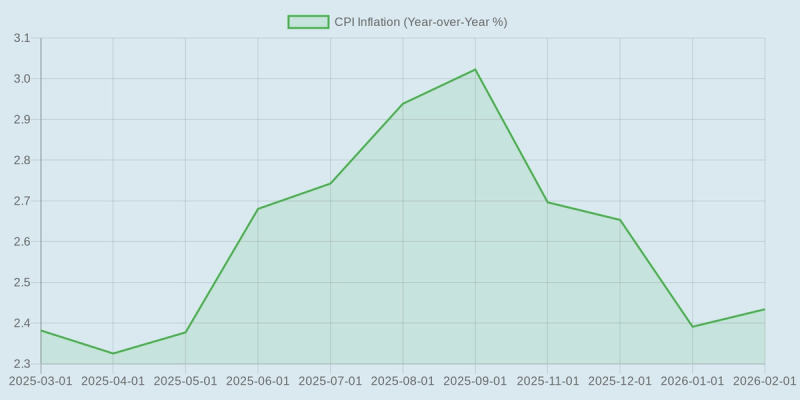

This energy shock is already complicating the macroeconomic picture for the Federal Reserve. High fuel costs act as a regressive tax on the consumer, sparking stagflation fears while the housing market is reportedly "in its own recession." If the energy spike embeds itself into broader goods and services, the central bank will be entirely boxed in—unable to cut interest rates to support slowing growth because of sticky inflation. As the chart below illustrates, year-over-year consumer price trends remain highly sensitive to these commodity supply shocks.

Looking ahead, volatility will be the only constant. Investors must closely monitor the upcoming weekly API and EIA Crude Oil Stock Changes starting in early April 2026, alongside CFTC speculative net positioning updates. More importantly, mid-April's U.S. Retail Sales and CPI reports will confirm whether this energy-driven inflation is officially eroding retail purchasing power. Until the geopolitical dust settles, domestic energy equities will likely remain a necessary, albeit volatile, portfolio hedge.