As the May 15 expiration of Jerome Powell’s term as Federal Reserve Chair approaches, the financial landscape is aggressively repricing the boundary between fiscal and monetary policy. President Trump’s nominee, Kevin Warsh, is heading into a highly contested Senate Banking Committee confirmation hearing this week with a pointed message: the Fed must "stay in its lane."

While Warsh is pledging to keep interest rate decisions strictly independent, his prepared remarks open the door to closer coordination with the White House and Congress on non-monetary matters. For investors, this shift away from the central bank's entrenched status quo is acting as a powerful catalyst for a theme that has been quietly building momentum across global markets: the Monetary Debasement Hedge.

Redefining the Central Bank's Core Mission

Warsh’s confirmation platform centers on trimming the Fed’s peripheral focus—specifically criticizing recent forays into climate policy and broader social goals—to return to the Federal Reserve's core economic mandate. In prepared remarks released ahead of his April 21 Senate hearing, his critique of the institution as "prone to inertia" and his willingness to break from standard operations have intensified a growing narrative of fiscal dominance.

With political leaders openly demanding lower interest rates to ease the burden of sovereign debt, markets remain sensitive to any perceived weakening of the central bank's inflation-fighting armor. The administration's vocal preference for aggressive rate cuts—with President Trump advocating for levels as low as 1%—has sparked anxiety that borrowing costs may be suppressed to accommodate federal spending levels.

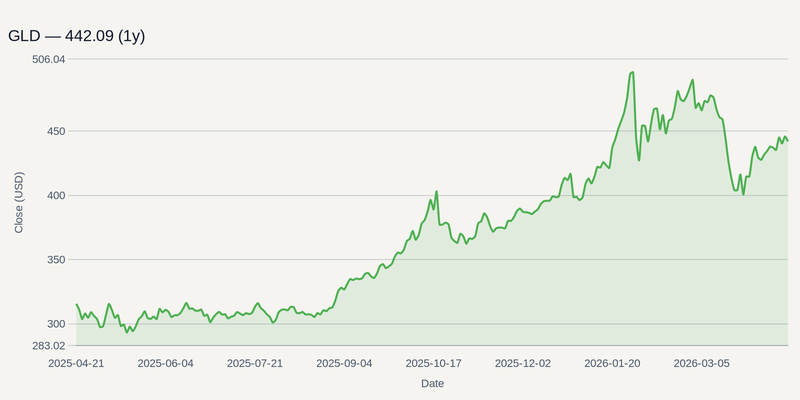

Fiscal Dominance and the Institutional Hard-Asset Bid

This exact friction between political expediency and monetary independence is driving a structural rotation into hard assets. Capital flows indicate that reserve managers and institutional funds are rapidly accumulating precious metals as a shield against potential currency devaluation, with the World Gold Council forecasting central bank demand to reach approximately 850 tonnes in 2026.

As the chart above illustrates, this institutional accumulation has supported a strong upward trajectory in physical gold over the past year, with prices rising more than 40% since April 2025. Although the metal has entered a period of consolidation following its January peak of nearly $5,600, the momentum is backed by aggressive Wall Street forecasting. Major banking desks, including J.P. Morgan and Wells Fargo, project gold prices could reach between $5,400 and $6,300 per ounce by the end of the year. Financial media coverage heavily features the narrative of fiat vulnerability, signaling what is becoming a highly convicted, albeit potentially crowded, consensus trade as Kevin Warsh heads into his Senate confirmation hearing on April 21.

The Hawkish Wildcard in the Nomination

The dominant market assumption is that a Trump-appointed Fed Chair will inevitably capitulate to dovish political pressure, but that outlook ignores Warsh’s actual track record. Historically an inflation hawk, Warsh explicitly notes in his prepared testimony—released April 20 ahead of his confirmation hearing—that low inflation is the Fed’s "plot armor" and that recent price surges have inflicted "grievous harm" on the public.

If Warsh successfully navigates a potentially deadlocked Senate Banking Committee and asserts strict, hawkish independence upon taking office, the current debasement narrative could face an abrupt reality check. A newly installed Fed Chair actively resisting pressure to cut rates would likely trigger a sharp strengthening of the U.S. dollar and a spike in real yields. Furthermore, any sudden resolution of global geopolitical conflicts or meaningful legislative action to reduce sovereign fiscal deficits could rapidly drain the risk premium currently baked into precious metals.

Positioning for a Shifting Macro Regime

For now, the policy ambiguity heading into May is funneling sustained capital into the Materials sector, specifically toward metals and mining equities that benefit from an inflationary or debasement backdrop.

Investors looking to capture this structural shift are prioritizing GLD for direct, unleveraged exposure to physical gold as a primary safe-haven asset. Beyond physical metals, the capital is flowing down the risk curve into operational vehicles. NEM (Newmont Corporation) remains a primary institutional vehicle, positioned to capture expanding profit margins as structurally higher precious metal prices outpace mining costs. Meanwhile, high-margin streaming companies like WPM (Wheaton Precious Metals) are providing investors with leveraged exposure to both gold and silver upside, insulating them from the direct operational risks and capital expenditures associated with traditional mining operations.