Wall Street pushed higher on Wednesday, with the QQQ heavily-weighted Nasdaq adding 0.77% and the S&P 500 climbing 0.54%. Despite the green on the screens, aggregate investor sentiment remains staunchly neutral. This divergence—prices drifting upward while conviction stalls—tells the story of a market waiting for the next definitive macroeconomic shoe to drop as we close out the first quarter of 2026.

The primary driver of this holding pattern is the Federal Reserve's current tightrope walk. With early 2026 inflation prints showing a stabilization rather than a rapid decline to the 2% target, market participants are heavily reliant on instruments like the CME FedWatch Tool to handicap the central bank's next move. Institutional capital is treating the current landscape as a "no-news-is-good-news" environment, allowing risk assets to float higher on light catalysts.

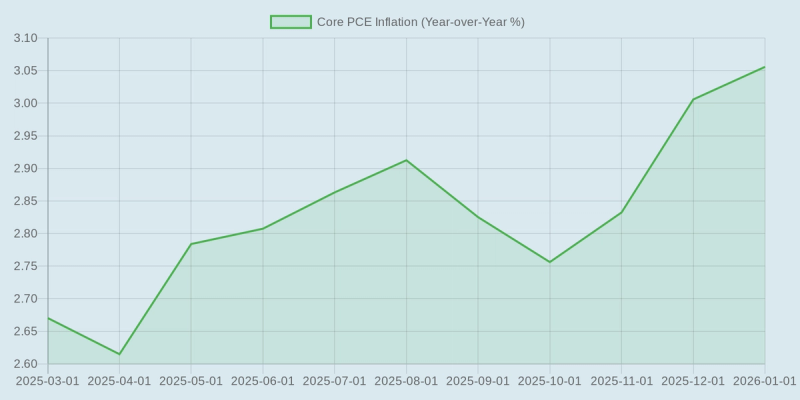

As the chart below illustrates, the recent trajectory of core PCE inflation over the last year has kept policymakers cautious, preventing a rapid pivot to aggressive easing.

In a regime where rates remain stable but the timeline for cuts gets pushed further down the calendar, Information Technology and Consumer Discretionary have maintained their leadership roles. The logic is straightforward: large-cap tech companies have the fortress balance sheets required to self-fund, insulating them from the immediate impacts of extended borrowing costs. Meanwhile, Financials are navigating a complex yield curve environment, balancing the benefits of higher net interest margins against the localized risks of loan defaults if the economy slows.

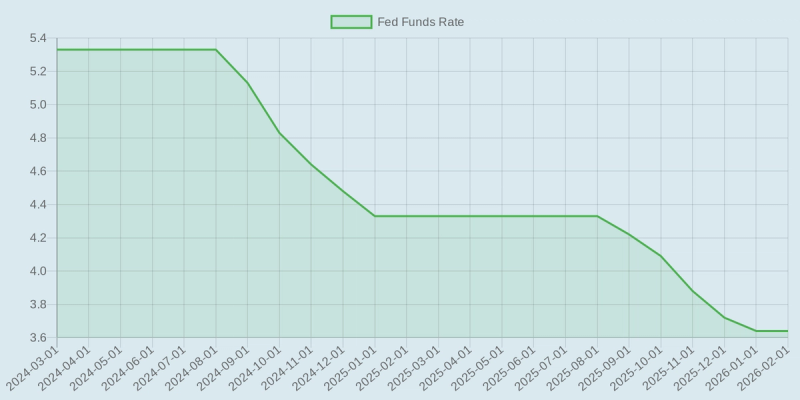

The Fed Funds rate, shown over the past two years below, highlights the sustained plateau that continues to dictate capital allocation across these major sectors.

However, the main threat to this low-volatility, upward-drifting environment is market complacency. The bearish counter-narrative argues that current equity valuations are pricing in a flawless soft landing with zero margin for error. If upcoming April labor data or Q1 corporate earnings—tracked closely by analysts at FactSet—show unexpected margin compression from sustained high operational costs, this "neutral" sentiment could rapidly shift to risk-off, triggering a swift repricing across major indices.

For now, the path of least resistance remains cautiously upward. Investors looking for an edge as Q2 approaches might consider barbell strategies: maintaining exposure to cash-rich Information Technology names while scouting for rotational value in Industrials and Materials, sectors that stand to benefit most if the broader macroeconomic resilience holds firm through the spring.