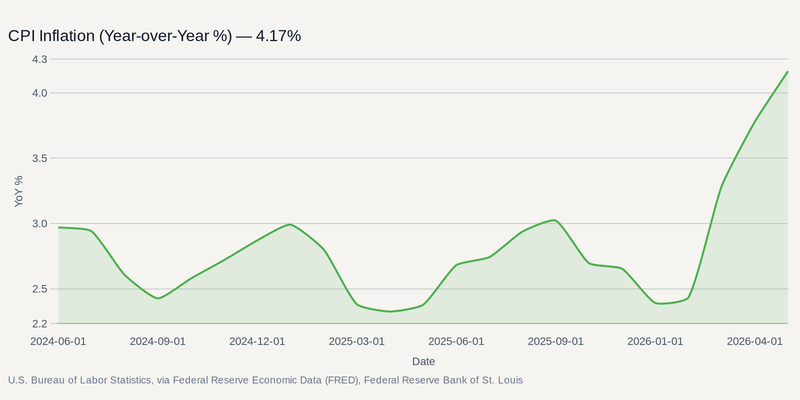

The U.S. economy is no longer just weathering a temporary supply disruption—it is structurally repricing. May consumer prices rose 0.5% today, lifting the headline inflation rate to 4.2% year-over-year. That marks the highest annual rate since April 2023. The White House insists the energy shock from the Iran War will fade once hostilities end. But institutional capital is positioning for a permanent shift: a geopolitical regime that guarantees higher neutral interest rates and ends the low-volatility era .

Markets spent the spring hoping strong jobs data would buy enough time to absorb surging crude. Instead, today's print confirms the labor market cannot shield the economy from the double blow of high borrowing costs and soaring energy bills .

Warsh’s baptism by fire

Newly sworn-in Federal Reserve Chair Kevin Warsh faces his first rate-setting meeting next week holding a weak hand. President Trump shrugged off the price spikes on Wednesday, famously declaring he "loves" the inflation because he expects crude to crash once the war concludes and military operations neutralize Iranian threats.

But central banks cannot underwrite policy on the promise of a forthcoming peace treaty. Core inflation—which strips out food and energy—remains elevated at 2.9%. While Warsh spent late 2025 arguing that artificial intelligence productivity gains justified rate cuts, that thesis is dead on arrival this summer. Markets now overwhelmingly favor the Fed holding its benchmark rate steady at 3.5%–3.75%. Rate cut expectations have collapsed, and European markets are already pricing in a new structural hiking cycle driven entirely by energy dynamics .

The cracks in traditional allocation

Markets have started to price in a more stubborn inflation backdrop, helped by tariff pressures and ongoing supply bottlenecks . That is putting pressure on the old playbook. Some institutional allocators are now openly arguing that the low-rate, low-volatility beta trade is behind them .

Capital is rotating away from plain-vanilla equities and longer-duration bonds. In their place, investors are leaning into floating-rate debt, private credit, and hard assets as they try to protect returns from margin pressure in consumer-facing sectors.

There is a trapdoor in that story. If geopolitical fears ease—say, through a meaningful diplomatic breakthrough in the Persian Gulf—the risk premium built into crude could shrink fast. In that case, central banks might also sound less hawkish, leaving crowded yield trades exposed. But unless shipping through the Strait of Hormuz becomes clearly safer, that is still a lower-probability outcome.

Upstream cash flows and floating-rate alpha

In a higher-for-longer regime defined by scarce raw materials, alpha concentrates at the very beginning of the supply chain and inside specialized credit.

Premier Energy operators are capturing massive cash flow tailwinds. XOM and EOG are positioned to outpace operating cost inflation through strict capital discipline and robust upstream margins. Meanwhile, as exploration budgets expand to meet structural supply shortages globally, top-tier infrastructure proxies like SLB transition from cyclical trades to mandatory holdings.

Beyond the wellhead, the capital rotation heavily favors credit-focused financials. Mega-cap diversified banks like JPM continue to leverage sustained net interest margin benefits while navigating the volatile crosscurrents. The most aggressive shift, however, is toward alternative asset managers and business development companies (BDCs). BX is perfectly structured to absorb the institutional capital abandoning traditional 60/40 models, while ARCC generates enormous, immediate yield from floating-rate debt that benefits directly from the Fed's inability to ease.

Investors will get clarity on this regime shift over the next eight weeks. June's FOMC press conference will confirm the new neutral rate, followed closely by Q2 upstream energy earnings. If those producers prove their margins are immune to localized cost inflation, the rotation out of tech and into hard assets will accelerate.