U.S. equities have officially logged a fourth consecutive week of losses as the escalating military conflict in the Middle East continues to roil global energy markets. With Brent crude crossing $107 a barrel and the effective blockage of the Strait of Hormuz threatening 20% of global oil supply, the macro environment has shifted violently. The small-cap Russell 2000 index is the first major benchmark to crack, falling more than 10% from its recent highs into correction territory.

But beneath the headline indices, a distinct rotation is taking place. Faced with a stagflationary threat, institutional capital is pivoting toward Retail Resilience Amid Geopolitical Conflict. Investors are simultaneously seeking refuge in defensive Consumer Staples that can weather consumer squeezing and domestic Energy producers insulated from Middle East crosshairs.

The Macro Domino Effect: From Oil to the Fed

The causal chain driving this market is straightforward but severe. Strikes on international energy infrastructure—including the devastating hit to Qatar's Ras Laffan liquefied natural gas (LNG) hub—have severely constrained supply. Following the early March API crude stock data, which confirmed rapidly tightening inventories, U.S. gas prices have surged toward $4 a gallon nationally, according to AAA.

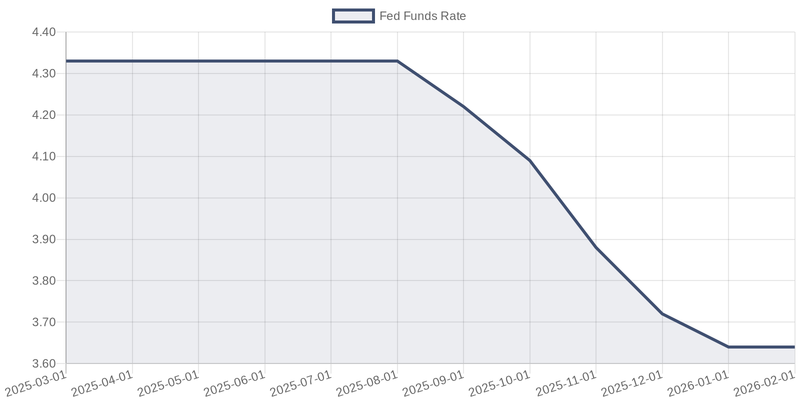

This energy shock directly threatens to re-accelerate inflation, effectively cornering the Federal Reserve. Any remaining optimism for imminent rate cuts in 2026 has evaporated. In fact, traders are now pricing in a higher probability of a rate *hike* than a cut by year-end, according to the CME FedWatch tool.

As the chart below illustrates, the prolonged plateau in the federal funds rate reflects the central bank's inability to loosen policy while supply-side inflationary pressures run rampant.

Higher yields have historically acted as a gravitational pull on growth valuations, which explains why the tech-heavy Nasdaq dropped 2% on Friday and the Russell 2000 entered a technical correction. Smaller, cyclical companies simply cannot absorb the dual headwinds of higher borrowing costs and margin-compressing energy prices.

The Scouter Edge: Retail as the Ultimate Bunker

While the VIX briefly spiked above 35 reflecting short-term panic, Scouter AI data identifies a powerful underlying theme with a trend score of 22: the rotation into large-cap retail bellwethers.

During recent "Retail's Big Week" earnings, sector leaders like Costco Wholesale Corporation, Walmart Inc., and Target Corporation proved their ability to maintain margins and grow foot traffic despite the inflationary squeeze on consumers. As gas prices eat into disposable income, the consumer's pivot to value and bulk purchasing structurally benefits these specific retailers. They operate as defensive safe havens that pass the consumer health check even when the broader economy is struggling.

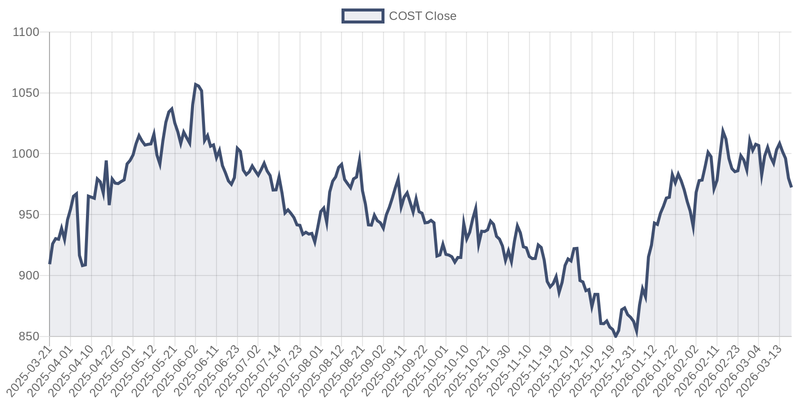

The chart below highlights the recent market action for Costco, illustrating how defensive retail staples are catching bids as investors rotate out of high-beta tech and small caps.

Domestic Energy: The Structural Winners

Beyond retail, the other half of this defensive barbell strategy relies on U.S.-based energy names. The disruption at Qatar's Ras Laffan facility has created a massive structural void in the global LNG market.

Consequently, U.S. pure-play liquefaction names like Cheniere Energy and NextDecade Corp. have surged as international buyers scramble to secure reliable Gulf Coast exports. Meanwhile, established giants like Exxon Mobil Corporation continue to serve as the standard hedge against prolonged supply disruptions in the Strait of Hormuz.

The Contrarian View: What Breaks the Thesis?

The primary risk to this defensive posture is a sudden geopolitical de-escalation. If a diplomatic breakthrough forces a reopening of the Strait of Hormuz, the geopolitical premium on crude would vanish overnight. Oil prices would likely crater back toward the $70 range, providing instant relief to inflation expectations. In that scenario, the market would rapidly price rate cuts back in, triggering a violent short-covering rally in the Russell 2000 and a rotation out of the defensive retail names that are currently outperforming.

Conversely, if oil spikes past $130, the resulting demand destruction could become so severe that even Walmart and Costco begin to see volume declines as consumers default to absolute bare-minimum survival spending.

Actionable Takeaway

For now, the market is treating the Middle East escalation as a lasting regime shift rather than a transient headline. Investors should monitor upcoming April releases of U.S. CPI data to gauge exactly how much of the energy spike is bleeding into core inflation. Until the Fed gets the all-clear on energy prices, the most prudent positioning remains barbell: domestic Energy equities to hedge the geopolitical risk, and high-quality, large-cap Consumer Staples to weather the resulting economic slowdown.