President Donald Trump is moving to aggressively intervene in agricultural markets today, signing dual executive orders aimed at crushing record-high beef prices and rebuilding a U.S. cattle herd that has withered to a 75-year low . With ground beef hitting a record $6.75 per pound earlier this year—a nearly 16% annualized surge—the administration is temporarily suspending tariff-rate quotas on all beef-exporting nations and rolling back endangered species protections that cattle ranchers argue inflate operational costs.

While the political theater centers on the meat aisle, a much quieter and highly lucrative dynamic is unfolding elsewhere in the grocery store. For the broader Consumer Staples sector, a massive wave of Defensive Margin Expansion is taking root, rewarding capital that rotates away from raw protein and into packaged foods.

The DOJ Squeeze on Meatpackers

The White House's protein focus has put the large beef packers—Tyson, Cargill, JBS, and National Beef—under sharper political and regulatory scrutiny. Those firms account for a very large share of U.S. beef processing, and the industry has also faced reported antitrust attention from the Department of Justice. With the administration publicly pressing processors over food prices, the protein sub-sector faces a mix of political scrutiny and already-tight cattle supplies.

Years of drought across Texas and the Great Plains have forced ranchers to reduce herds, tightening domestic supply. Imports can help offset some of that pressure, but they do not quickly reverse the structural herd losses that have built up over time. Downstream buyers are already feeling the strain, with restaurant and fast-casual operators exposed to high beef costs seeing margin pressure as wholesale prices remain elevated.

Soft Commodities Flip to Surplus

Conversely, packaged Food Products manufacturers have generally benefited from prior rounds of price increases and, in some cases, easing input costs. Over the past two years, many companies raised retail prices to offset supply-chain disruptions and higher agricultural input costs.

Now, parts of the soft-commodity backdrop are moving more in their favor, although the picture is mixed rather than uniformly surplus. Sugar has eased from prior highs, while cocoa and coffee remain volatile and have not both clearly shifted into a durable surplus. Because many of the retail price increases from 2024 and 2025 have remained in place, lower input costs can support margins where they occur.

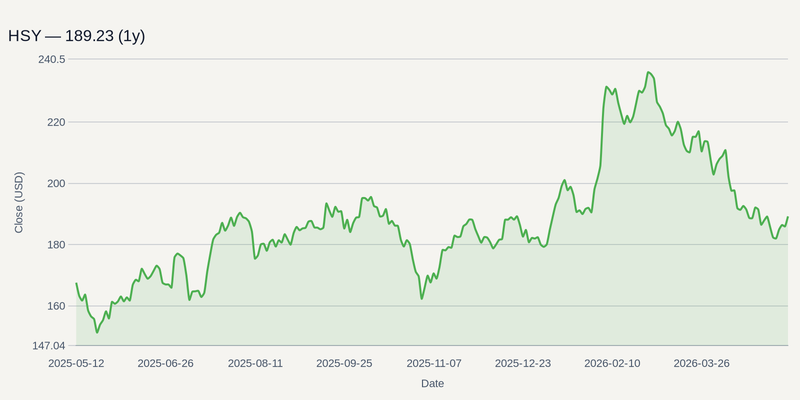

This setup can benefit confectioners and snack manufacturers. The Hershey Company (HSY) may see relief if cocoa and sugar costs continue to normalize, though the stock’s outlook still depends on pricing, volumes, and broader cocoa-market conditions. There is no clear evidence of a broad DOJ price-gouging probe targeting packaged-food companies in general, and any claims about merger activity or private-equity deployment should be treated as company-specific rather than sector-wide.

Appetite Suppressants and Consumer Exhaustion

The golden era for packaged food margins is not without structural friction. One persistent overhang is the adoption of GLP-1 weight-loss medications, which some companies and analysts say is weighing on demand for calorie-dense snacks and sugary treats. Top-line volume growth remains sluggish in many categories, so firms have often relied more on pricing and margin recapture than on unit growth.

Furthermore, consumers appear stretched. Slower discretionary income growth and price sensitivity may limit how much more grocery producers can pass through if another supply shock hits. Climate volatility and new compliance requirements, including the European Union Deforestation Regulation, also could add long-term supply-chain friction just as margins peak.

Navigating the Shelf Space

With second-quarter 2026 earnings approaching in July, investors are still treating large food and beverage names as relatively defensive, even as capital rotates toward companies seen as better able to adapt to changing consumer preferences and manage costs.

PepsiCo Inc. (PEP) has been leaning into convenience formats and beverages marketed around hydration and added protein, though any claim that this alone is offsetting GLP-1-related pressure is too strong based on public disclosures. Meanwhile, Keurig Dr Pepper Inc. (KDP) continues to rely on partnerships and channel expansion to support growth, and Utz Brands Inc. (UTZ) has been working to improve efficiency and margins in its salty-snack business. Investors tracking this divergence should watch upcoming crop and commodity updates later in the summer, which could influence input costs for packaged-food companies, especially those exposed to cocoa and other agricultural ingredients.