On Monday, headlines captured a perfect snapshot of aerospace's existential divide: a commercial drone manufacturer declared an autonomous "arms race" just as legacy prime Sikorsky confirmed it would bankroll a VIP helicopter landing pad at the White House. The dichotomy frames a multi-year procurement shift where traditional, high-margin legacy platforms are suddenly competing for oxygen against asymmetric, attritable autonomous systems.

Geopolitical heat has pushed industry revenues past $1 trillion for the first time . But this isn't just a rising tide lifting all ships. The anticipated $1.5 trillion defense budget from the Trump administration isn't simply buying more of the old stuff; it is actively funding a structural "Security Supercycle" focused on modernization and strategic stockpiling .

The Multi-Year Backlog Shield

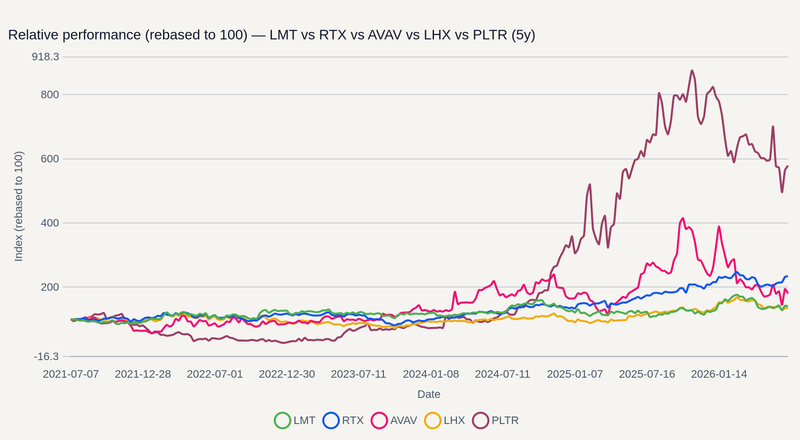

Legacy defense primes are currently sitting on unprecedented order books. LMT is heading into its July earnings ready to detail the multi-year momentum from a newly awarded $35 billion THAAD interceptor contract (which, in defense-contracting terms, is basically a seven-year license to print cash) . Meanwhile, RTX is prepping corporate updates on its $515 million SPY-6 naval radar build-out .

These massive, execution-heavy contracts help establish a fundamental valuation floor in our risk models, even as supply chain bottlenecks and talent constraints persist . But legacy platforms that fail to align their technology investments with agile capital priorities face a looming risk. Capital is beginning to relentlessly reallocate toward pure-play autonomous platforms and dual-use innovations .

Scaling the Asymmetric Fleet

The rapid scaling of uncrewed tech is rewriting unit economics for the Department of Defense. Rather than relying solely on exquisite, multi-decade development cycles, the Pentagon is pivoting to attritable systems (hardware cheap enough to lose in combat without sinking the balance sheet).

For investors conducting diligence on this space, AVAV is a key case study. The company recently secured a massive $500 million counter-drone IDIQ (Indefinite Delivery, Indefinite Quantity) contract from the U.S. Army—with the first $80.5 million task order already dropping in early July (because nothing says "operational urgency" like a holiday-week contract release) . Software is the invisible transmission mechanism here. Companies like PLTR and LHX are capturing the transition toward software-defined defense architectures. This thematic shift across the Aerospace & Defense sector is already triggering accelerated inflows into related ETFs as the market sniffs out the pivot to agentic AI .

Navigating the FY27 Appropriations Roadmap

To be clear, legacy primes aren't dead money. Autonomous systems are impressive in skirmishes, but pacing threats still require heavy metal and deep manufacturing bases. A software overlay can't replace the kinetic deterrence of a fully funded THAAD battery.

Yet, the real test of this bifurcation will surface in September 2026, as the Fiscal Year 2027 defense budget deadline forces Congress to negotiate specific appropriations for agentic AI and autonomous systems (or, more likely, kick the can with a continuing resolution while the real horse-trading happens behind closed doors) . For anyone doing diligence on traditional industrials, this budget isn't just a spending bill—it's a critical roadmap to help assess which platforms survive the hardware-to-software transition, and which ultimately get stranded on the helipad.