Fortifying the perimeter

On July 15, the Senate Commerce Committee is scheduled to vote on a bipartisan push to toughen the U.S. government's ban on Chinese automakers entering the American market. Today, the head of the National Highway Traffic Safety Administration (NHTSA) demanded that autonomous vehicle operators immediately address a clear pattern of driverless fleets interfering with emergency responders (which, to be fair, is a polite way of saying "stop blocking ambulances"). This is not standard political theater or isolated regulatory housekeeping. Washington is methodically turning vehicle hardware and software into a strategic choke point.

By leveraging overlapping trade restrictions and safety mandates, regulators are attempting a massive market rewiring. The goal is straightforward: make autonomous vehicle deployment slower and more domestically controlled, while building a legislative moat against low-cost foreign electric vehicle competition. For investors, this means the Domestic Auto Protectionism trend is no longer just a headline risk, but the fundamental constraint dictating the sector's cost structure for the next several quarters.

The collateral damage of onshoring

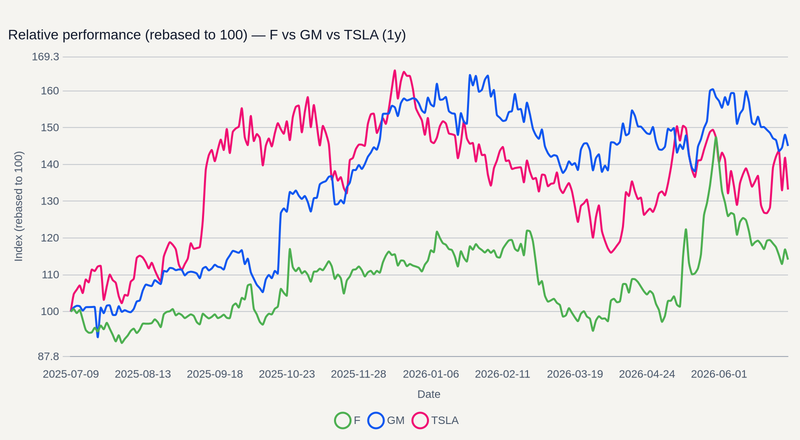

Aggressive trade barriers were supposed to force a domestic manufacturing renaissance, heavily favoring stateside original equipment manufacturers and labor. But that thesis is facing a brutal stress test as reality bites back on the factory floor. Legacy heavyweights like F and GM are watching their expected profits bleed out by the billions as tariffs trigger massive cost spikes for essential imported parts and factory robotics .

Compounding the margin erosion, the protectionist firewall just took a severe structural hit from the judicial branch. The U.S. Supreme Court issued a major decision earlier this year invalidating the emergency global tariffs that the administration aggressively rolled out under emergency powers over the past year . But while the ruling struck down those broad emergency-power levies, it left the critical Section 232 tariffs on steel, aluminum, and imported vehicles and parts firmly in place—meaning the core supply-chain pain remains largely unresolved. This rollback underscores exactly how fragile executive-branch trade remedies are when they collide with established federal law .

The transatlantic spillover

The friction is not contained to the Pacific. While the EU narrowly dodged a threatened 25 percent auto tariff by rushing to implement the Turnberry trade deal just ahead of the administration's July 4 deadline , the resulting 15 percent import levy (which went into effect July 1) still places premium manufacturers like BMWYY squarely in the crosshairs of global trade friction. (Because nothing says "stable planning environment" like negotiating multi-billion-dollar supply chains via Truth Social posts.)

The timing is exceptionally punitive. These trade pressures arrive just as Brussels reviews its own complex automotive policies, including the highly contested 2035 phase-out of combustion engines. It is a massive game of chicken that threatens to fracture global automotive supply lines right as the industry attempts a highly capital-intensive platform transition.

Rewiring the continental supply chain

With the U.S. formally declining to extend the USMCA on July 1—triggering a grueling cycle of annual reviews instead of a clean 16-year renewal (because why settle for stability when you can have perpetual leverage?)—focus shifts to the third quarter's imminent bilateral trade talks . The next round of negotiations kicks off the week of July 20 in Mexico City, specifically targeting cross-border automotive rules of origin and pulling suppliers directly into the blast radius.

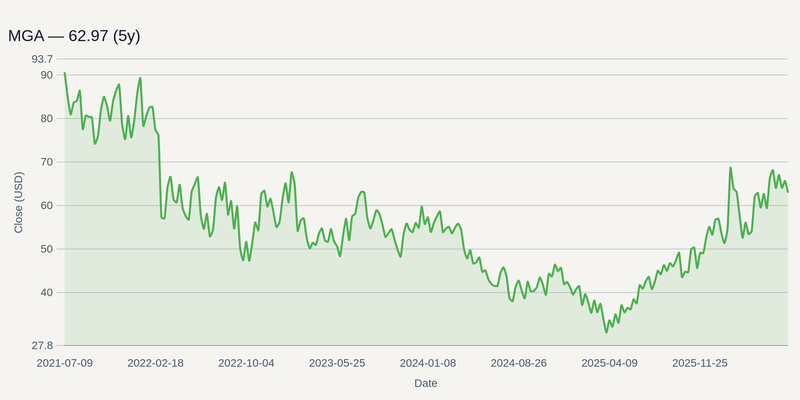

Major parts suppliers like MGA are exceptionally vulnerable to these renegotiations. Their entire operating model relies on a seamless, cross-border dance where a single component might cross North American borders multiple times before it ever meets a chassis. The primary risk to the bullish onshoring narrative is that the domestic manufacturing base simply cannot scale fast enough without foreign components, forcing a sudden relaxation of these barriers to prevent an inflationary consumer revolt. Until then, the regulatory wall remains the dominant force sorting the winners from the structurally impaired.