Against a backdrop of broader market chop today, a stark divergence is playing out within the Financials sector. Traditional retail property and casualty (P&C) carriers are facing escalating state-level scrutiny, while specialized players are quietly engineering a golden age of underwriting profitability.

The immediate catalyst for the sector's regulatory overhang comes out of California, where the Department of Insurance said it is seeking penalties against State Farm. The state alleges the carrier mishandled, delayed, and underpaid claims stemming from the January 2025 Los Angeles wildfires. Yet, while retail sentiment remains cautious as rising consumer premiums create friction, institutional capital is aggressively rotating toward a new structural theme: AI-Optimized Alternative Capital Insurance.

The Regulatory Reality Check in California

The State Farm enforcement action announced by California regulators on May 4, 2026—seeking record penalties for the mishandling of claims following the 2025 Los Angeles wildfires—underscores the persistent threat of what the industry terms "social inflation." While social inflation specifically refers to the surge in litigation expenses and outsized jury awards, it is being compounded in California by stringent regulatory oversight and the structural reality of increasingly severe climate catastrophe claims. For carriers highly exposed to standardized personal lines in catastrophe-prone states, balance sheet stability is under constant siege.

However, focusing solely on the California regulatory thicket misses the broader institutional rotation. The reality is that while broader property and casualty markets are facing softening property pricing and rising competition in 2026, California’s specific risk profile keeps it largely decoupled from the national trend. To combat this, the smartest capital in the room is bypassing mass-market quagmires and pivoting toward specialized commercial lines and algorithmic efficiency.

Algorithmic Underwriting and the Margin Renaissance

Despite the headline headwinds, the broader Insurance sector is successfully leveraging advanced artificial intelligence and digital optimization to achieve robust underwriting margins that, for industry leaders, are reaching multi-year highs. AI efficiency gains—particularly in "agentic" risk assessment and straight-through processing—are allowing carriers to accurately model complex risk distributions, reducing operational bloat and sustaining profitability even as they navigate regulatory transitions in volatile markets.

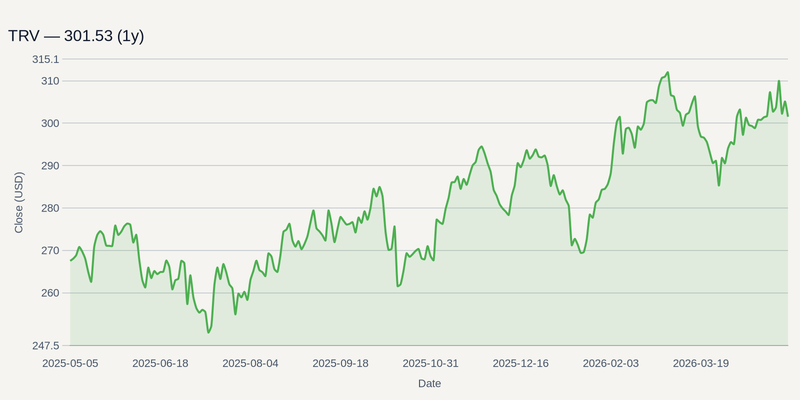

Names like The Travelers Companies Inc. (TRV) are illustrating exactly how strong pricing power, combined with significant capital return—including $1.8 billion in open-market share buybacks in Q1 2026—can drive robust EPS growth. By optimizing their book dynamically rather than relying purely on volume, prime carriers are isolating themselves from the localized friction and inflationary pressures still affecting legacy personal lines.

Similarly, Chubb Limited (CB) has strategically insulated its balance sheet by focusing on specialized commercial and high-net-worth personal lines, the latter of which maintained a 92% renewal retention rate in the first quarter of 2026. These segments command superior profit margins and remain less vulnerable to the rigid, state-by-state regulatory gridlock that has historically hampered standard homeowner policies, even as carriers begin to pilot California's new Sustainable Insurance Strategy framework.

Alternative Capital as a Structural Buffer

Optimism around tech-driven efficiency is high, but it is balanced by a realistic understanding of market softening and the broader macroeconomic uncertainty tied to fluctuating interest rates. To boost investment yields while premium growth moderates, insurers are increasingly partnering with private capital through sidecars and insurance-linked securities (ILS).

This influx of alternative capital is driving targeted merger and acquisition activity across the space. RenaissanceRe Holdings Ltd. (RNR) has been a prime beneficiary of this dynamic, leveraging its Validus Re integration to drive high net investment income and fee-based revenue from its Capital Partners unit. Meanwhile, Ryan Specialty Holdings Inc. (RYAN) is heavily utilizing AI-led operational enhancements—specifically its "Empower" initiative—to bolster efficiency as property pricing softens, illustrating how structural improvements can help mitigate the impact of a cooling rate environment.

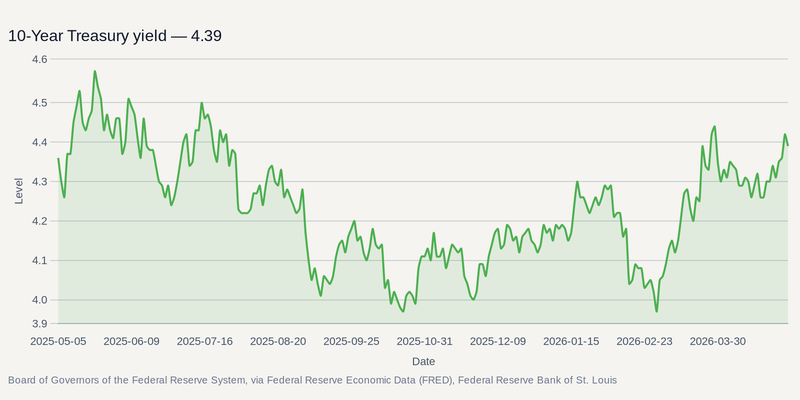

To understand the broader investment yield environment supporting these balance sheets, we have to look at the baseline borrowing costs that dictate carrier float returns .

Horizon Risks and Late-2026 Catalysts

The most significant risk to this bullish margin thesis is that medical cost inflation and broader macroeconomic volatility eventually overwhelm the efficiency gains extracted by AI. If alternative capital pulls back due to sudden yield shocks, the M&A engine supporting the sector's top players could stall.

Looking ahead, Scouter's catalyst data flags a potentially important sequence of events for the sector. Second-quarter earnings reports due in July 2026 could offer an early read on whether AI efficiency is offsetting softer property pricing. Any federal deregulatory policy changes later in 2026 would likely be a structural tailwind, and September 2026 is typically a busy period for pension risk transfer deal announcements. For investors, the playbook remains clear: avoid the heavily regulated, mass-market crosshairs and favor the specialized carriers that are pairing algorithmic underwriting with private capital.