The broader tape remains structurally bifurcated today, with the Information Technology sector lifting indices marginally while consumer discretionary and staples lag. Behind that divergence is a profound AI Infrastructure Capex Supercycle that is swallowing corporate budgets whole. Technology giants and hyperscalers are on pace to deploy over $700 billion in capital expenditures in 2026, transitioning from initial, specialized language-model training clusters to massive-scale inference networks. Corporate filings reveal these historic capital commitments are now dwarfing the telecom fiber build-outs of the late 1990s .

Pivoting from Training Clusters to Inference Networks

The current generation of data center architecture is widening rapidly. While NVIDIA Corporation established a multi-trillion-dollar market capitalization by providing the foundational graphics processing units, the ecosystem's constraints are evolving. Vast Data’s CEO recently reiterated that artificial intelligence disruption will force a restructuring of every major industry vertical, generating unprecedented demand for raw data throughput.

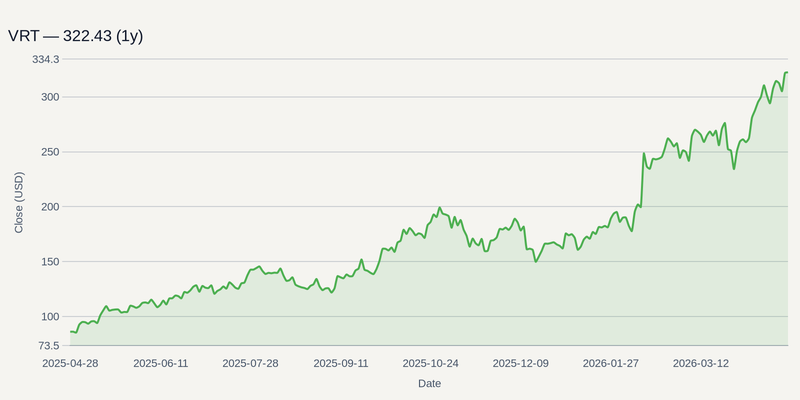

For companies scaling massive compute networks, these constraints—often described by Gabelli's John Belton as a "healthy bottleneck" for Big Tech—are shifting from silicon scarcity to power delivery and thermal management. High-density liquid cooling has become a non-negotiable line item, directly funneling infrastructure capital toward specialized providers like Vertiv Holdings Co.

The Software Monetization Air Pocket

Despite the sheer velocity of capital deployment, the infrastructure surge faces a distinct vulnerability. The primary risk to this hardware cycle is a potential capital expenditure "air pocket." If hyperscalers fail to generate the end-user software revenues required to justify their massive $700 billion investments, enterprise boardrooms could abruptly hit pause on future data center scaling.

Furthermore, the push for custom, in-house silicon by these same cloud giants poses a looming, long-term displacement threat to pure-play merchant silicon vendors. Geopolitics compounds this threat profile, as the acute risk of newly enacted export restrictions to China hovers over the entire semiconductor supply chain.

Custom Silicon and the June Catalyst Window

As the deployment cycle matures, hyperscalers are aggressively seeking alternative architectures to offset single-vendor reliance. Advanced Micro Devices is securing significant custom silicon deals to power these next-generation facilities, while Broadcom Inc. continues to lead the custom networking and application-specific integrated circuit (ASIC) space required to tie inference networks together.

This capital cycle will face an immediate reality check in late May 2026, when major semiconductor manufacturers report fiscal first-quarter earnings and update their forward capex guidance. Shortly after, the focus will pivot directly to software monetization at major developer conferences. Chief among these is Apple’s Worldwide Developers Conference on June 8, 2026, where consumer-layer AI integration will attempt to prove that the underlying hardware spend is ultimately justified by user adoption.