The unofficial de-escalation of the Iran conflict has removed a significant macro overhang, clearing the path for the Information Technology sector to resume its structural breakout. With the geopolitical risk premium temporarily deflated, the tech-heavy Nasdaq just capped a historic 13-day winning streak—its longest since 1992—surging 6.8% this week. Yet, beneath the headline celebration of a relief rally, institutional capital is rapidly repositioning for the next—and far more capital-intensive—phase of the AI infrastructure arms race.

The market is no longer merely buying the conceptual promise of artificial intelligence; it is financing a massive physical build-out. The shift from general-purpose computing to accelerated computing requires entirely new data center architectures. Earlier this month at the HumanX AI Conference in San Francisco, key infrastructure roadmaps were laid out, signaling that the industry is aggressively moving from pilot phases into full-scale production. For the Semiconductors & Semiconductor Equipment industry, this marks a distinct transition from hype to heavy lifting.

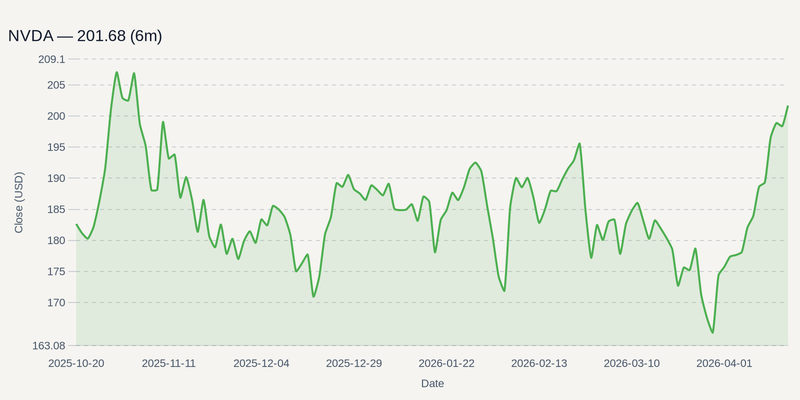

As the chart below shows, NVIDIA Corporation has recently broken out of a six-month consolidation range, as the market reaffirms its position as the primary provider of high-performance GPUs and full-stack AI computing platforms.

The company remains the undisputed anchor of this capital cycle, with the market intensely focused on the upcoming volume shipments of its next-generation Blackwell Ultra and Rubin-class server racks. But the supply chain required to deliver these architectures is growing increasingly complex. It relies heavily on Taiwan Semiconductor as the primary foundry capable of manufacturing advanced nodes at hyperscaler volumes, and Broadcom Inc. for the specialized high-speed networking components that stitch these massive clusters together.

Physical Bottlenecks and Grid Realities

The most immediate risk to this momentum isn't necessarily a lack of end-user demand, but the severe physical constraints of deploying it. The extraordinary energy requirements and logistical bottlenecks of multi-gigawatt data center clusters are beginning to slow physical deployment timelines, with "speed to power" becoming the primary metric for project viability. High-density accelerated computing, particularly for next-generation platforms like NVIDIA's Rubin, generates immense heat that creates a hard physical limit for legacy air-cooled data center facilities.

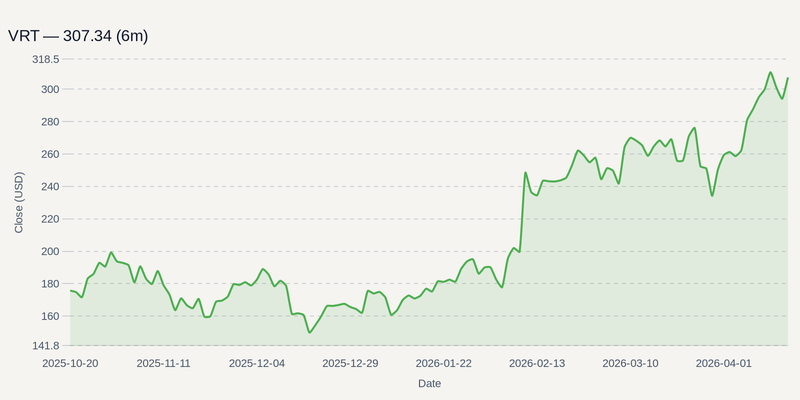

This bottleneck has driven a surge of capital toward critical infrastructure providers. The chart below illustrates the six-month trajectory of Vertiv Holdings, capturing the rising market premium placed on companies that supply essential liquid cooling and power management systems.

Without these thermal management solutions, the next generation of accelerated silicon literally cannot run at capacity. However, as capital expenditures by tech giants are projected to outpace revenue growth in the 2026 fiscal year—a trend highlighted by broader corporate expenditure data showing capex-to-revenue ratios reaching record highs for the "Big Five" hyperscalers—free cash flow across the tech ecosystem is coming under significant pressure. Corporate sentiment is currently ruled by a fear of missing out, forcing hyperscalers to aggressively invest in infrastructure despite the certainty of near-term margin compression.

The Production Gantlet

Over the next quarter, the market will demand proof that this unprecedented capex cycle is translating into sustainable enterprise value. Next month’s fiscal Q1 earnings from NVIDIA Corporation will provide crucial forward guidance on exactly how fast these high-demand AI server racks can actually be manufactured and deployed into facilities.

Looking further ahead, this July will serve as the ultimate litmus test when major hyperscalers, including Microsoft (Azure) and Amazon (AWS), report their calendar Q2 earnings. Investors are beginning to show growing skepticism regarding the tangible return on investment for generative AI services as adoption moves from trial to production. If cloud revenue acceleration fails to match the staggering pace of infrastructure spending, the broader Information Technology sector could face a harsh repricing. For now, the momentum remains fiercely tied to the companies building the specialized silicon, networking, and cooling pipes of the accelerated computing era.