The digital expansion of artificial intelligence is colliding with the physical reality of the supply chain. Overnight, Beijing stepped up export scrutiny on indium—a niche metal essential for producing the indium phosphide that powers next-generation AI data center optics. As the U.S. navigates a global AI arms race, control over the base layer of advanced materials has become a potent geopolitical weapon.

For Fed Chairman Kevin Warsh, this infrastructure build-out presents a structural test: decoding whether the massive capital expenditure required to secure these supply chains will ultimately cool aggregate price pressures through efficiency, or stoke them through raw material constraints. While broad indices are trading higher today, the underlying capital flows are migrating toward the heavy industrial players tasked with manufacturing these critical components.

The Sovereign Capital Backstop

The Advanced & Specialty Materials sector is undergoing a strategic shift driven by national security priorities and energy efficiency mandates. Governments are increasingly underwriting the massive capacity expansions required to onshore production.

Programs like India's Production Linked Incentive scheme are deploying direct financial support to boost domestic manufacturing of specialty steel and semiconductor components . In the U.S., Department of Energy grants are targeting similar supply chain bottlenecks, mitigating the risk for companies overhauling their operational footprints .

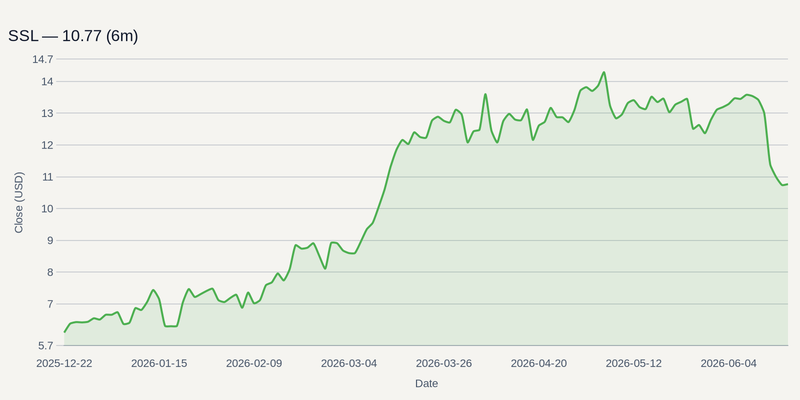

This sovereign de-risking allows legacy operators to deploy heavy CapEx with greater confidence. In early June 2026, SSL authorized a €60 million expansion at its Brunsbüttel site in Germany, specifically targeting advanced materials and specialty chemicals .

Bridging the Deep Science Funding Gap

The primary friction in next-generation composites is the duration of the research and development cycle. Deep science ventures require substantial upfront capital long before commercial monetization becomes visible .

For investors assessing 10,000+ tickers, the edge lies in identifying companies where capacity expansion aligns with immediate, high-margin end markets. SOLS, for instance, has anchored its revenue model on direct exposure to electronic, nuclear, and high-performance refrigerant markets, insulating its balance sheet from the cash drag of purely theoretical R&D.

Industrial Demand Masks Residential Weakness

While infrastructure and tech tailwinds are robust, the broader materials complex is wrestling with a bifurcated economy. The building products side of the industry faces structural drags from stagnant residential construction volumes.

Chart failed: Series "MORTGAGE30US" is not from an allowed public-domain source (source IDs on this release: 41). Allowed source IDs: 1, 4, 14, 18, 19, 22, 53.

Elevated financing costs continue to depress residential turnover, applying pressure on legacy insulation and architectural chemical lines. To survive the margin squeeze, providers like OC are doubling down on branded building products like high-efficiency insulation and roofing, having completed the divestment of its capital-intensive glass reinforcements business in April 2026. Similarly, HUN—which recently announced a merger of equals with Olin Corporation to form a $12-billion-plus chemicals leader—is rotating its portfolio focus toward aerospace materials and advanced polyurethanes, shielding its core revenue from the cyclical housing slump.

Margin Preservation Ahead of Q2

As the sector approaches the Q2 reporting window in late July and early August, the analytical focus shifts from growth narratives to capital discipline. Scouter data indicates that sentiment across the advanced materials space remains grounded in steady capacity utilization rather than retail speculation. Companies reporting over the coming weeks—including OC, HUN, and SOLS—will need to show whether pricing, mix, and cost control are enough to offset pressure from softer volumes in more cyclical end markets.